The year 2025 has marked a seismic shift in the global trade system toward protectionism, with the US introducing hefty new tariffs to shield domestic industries from foreign competition and to realign international trade in favour of US economic interests. On 2 April 2025, the US administration announced a baseline 10% tariff on imports from 185 countries, alongside higher country-specific tariffs of 17% to 49% on 83 countries that applied asymmetric tariff and non-tariff barriers to US exports, contributing to persistent trade deficits. EU countries, in particular, were initially hit with a 20% country-specific tariff.

The implementation of these higher tariffs has been repeatedly suspended, reflecting their use as leverage rather than as a permanent trade measure. The Executive Order signed by President Trump on 2 April 2025 provides for reduction of tariffs if US trading partners take substantial steps to address the US trade deficit. In this context, the US has pursued negotiations with a wide range of partners to address trade imbalances, with the EU, representing 18% of total US imports, emerging as a central focus of these discussions.

On 27 July 2025, the EU and US announced the conclusion of a framework trade deal. Under the deal, the US will impose a 15% import tariff on most EU goods. While this represents a notable increase from historical levels of 1–2%, it remains well below the higher tariffs the US had threatened over the previous four months. Concurrently, the EU has committed to importing $750 billion of US energy by 2028 ($250 billion annually), covering natural gas, oil, and nuclear fuels, alongside an additional $600 billion of investment in the US economy. According to the European Commission, the final volumes and the composition of oil, LNG, nuclear fuel, and related services will depend on factors such as commodity prices, exchange rates, and final investment decisions by project promoters, with actual outcomes ultimately determined by commercial transactions. The agreement is non-binding, creating no legal obligation for either side.

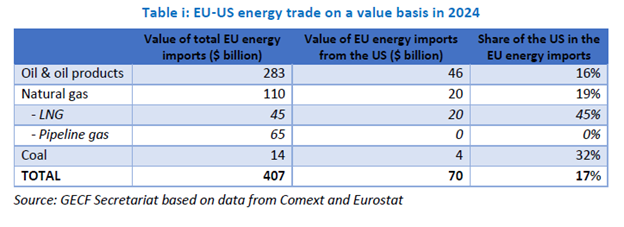

For context, the EU total energy import bill reached $407 billion in 2024, with natural gas accounting for $110 billion, or 27% of the total (Table i). The US supplied $70 billion worth of energy, representing 17% of total EU energy imports. On a value basis, the US accounted for 16% of EU oil and oil products imports, 45% of LNG imports, and 32% of coal imports (data on nuclear fuel excluded from this assessment). These figures illustrate the US major role in key segments of the EU’s energy import mix, particularly LNG. Achieving the ambitious targets set under the trade deal would require a substantial increase in US energy exports to the EU, rising from $70 billion in 2024 to $250 billion annually.

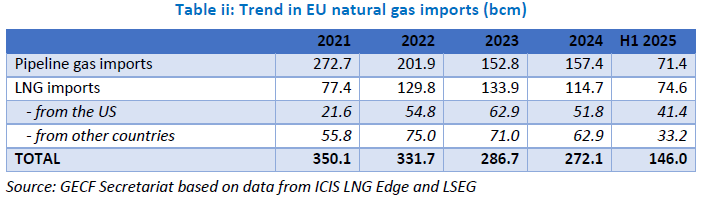

The trade deal is understood to focus primarily on natural gas. The expansion of EU LNG imports from the US, the EU’s main LNG supplier, is regarded as a strategic tool to achieve the targeted energy trade values. With domestic gas production limited, the EU continues to rely on imports for around 90% of its gas consumption. Although regional imports fell steadily from 350 bcm in 2021 to 272 bcm in 2024 as overall gas consumption declined, the composition of these imports shifted markedly in favour of LNG, driven by a sharp reduction in pipeline gas imports. Between 2021 and 2024, the share of pipeline gas in total EU consumption dropped from 70% to 50%, while LNG’s share rose from 20% to 40%. This transition enabled a substantial increase in LNG imports from the US, with its share of total EU gas imports rising from 6% to 19% and its share of LNG imports increasing from 28% to 45% over the same period (Table ii). The trend accelerated in the first half of 2025, when LNG imports surpassed pipeline gas imports in the EU for the first time. During this period, US LNG accounted for 28% of total EU gas imports and 55% of LNG imports, on track to reach record levels by the end of 2025. On a value basis, US LNG exports to the EU amounted to $20 billion in 2024.

There is broad recognition of the limited scope for increasing LNG imports from the US to the level required to meet the targeted rise in EU energy imports to $250 billion annually. The target appears highly ambitious, with both sides seemingly overpromising what can realistically be bought and sold, as a range of factors could constrain the feasibility of the trade deal.

First, the US currently has 105 Mtpa of operational LNG capacity, with an additional 115 Mtpa under construction and 100 Mtpa of planned capacity targeting FID. Assuming that most capacity from operational and under-construction projects is already contracted, largely by portfolio players, not more than 100 Mtpa, primarily from planned projects that are dependent on securing new long-term contracts, remains uncontracted and theoretically available for future deals. Even in an ideal scenario, supplying the full 100 Mtpa at current spot prices would generate only $60 billion annually for the US, well below the levels needed to make a meaningful contribution to the EU-US trade agreement. Moreover, since April 2025 several Asian countries have expressed interest in increasing LNG imports from the US to reduce their trade surpluses and investing in US LNG projects to secure offtake supply. Consequently, the actual volume of US LNG available for the EU will be much lower than the theoretical maximum.

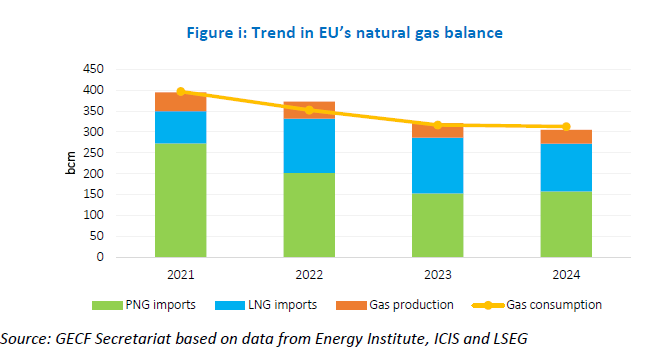

Second, the EU does not have sufficient gas demand to absorb additional LNG volumes from the US. Regional gas consumption fell sharply from 400 bcm in 2021 to 313 bcm in 2024, driven by a combination of structural and cyclical factors (Figure i). These include coordinated demand-reduction measures introduced in 2022 to mitigate the risks of gas supply disruptions, accelerated deployment of renewable energy, improvements in energy efficiency, and milder winter seasons that lowered heating demand. Looking ahead, gas demand in the EU is expected to remain flat or even decline slightly through 2030, which could significantly constrain the scope for a major expansion of US LNG supply to the EU market.

Third, the EU total LNG import capacity reaches 250 bcma (185 Mtpa), with 13 Member States equipped with regasification infrastructure. Notably, between 2022 and 2024, the EU commissioned a record 12 new LNG terminals and completed 6 expansion projects, collectively adding 70 bcma of capacity. However, capacity utilization rates remain around 50%, primarily due to regional bottlenecks, especially limited gas interconnection infrastructure. For example, Spain has the largest regasification capacity in the EU, but insufficient pipeline connections with neighbouring countries restrict its ability to distribute LNG across regional markets. These limitations may constrain the growth of US LNG supply.

Fourth, nearly all pipeline gas imports and around 60% of LNG imports in the EU are tied to long-term contracts and are not easily redirected. With EU gas demand showing little growth potential, the primary avenue for scaling up US LNG exports lies in substituting spot and short-term LNG volumes from other suppliers. In 2024, approximately 40% (48 bcm) of EU LNG imports were sourced on a spot or short-term basis, but a large share of this already came from the US due to its contractual flexibility, limiting the scope for further increases in US LNG supply.

Fifth, while EU and US authorities can facilitate connections between buyers and sellers, the final commercial decisions rest entirely with private companies. The EU cannot compel firms to prioritise US energy purchases, regardless of market conditions. Companies base their decisions on profitability, market dynamics, and long-term risks, with governments able only to signal support or provide incentives. Even with strong political backing, it is ultimately commercial considerations that determine whether contracts are concluded, making business incentives the decisive factor in shaping market outcomes.

Sixth, a central tension arises from reconciling the EU’s short-term commitment to expand US LNG imports with its long-term climate objectives. The EU has pledged steep emissions reductions and a rapid phase-out of fossil fuels, yet locking in large volumes of US gas could entrench dependency that conflicts with its net-zero ambitions. In particular, the EU methane regulation adds another layer of complexity and may hinder US LNG imports growth. For the US, such an agreement would secure markets for its growing LNG capacity, but for Europe it could undermine climate credibility, increase the risk of stranded assets, and complicate the clean energy transition intended to support sustainable economic growth.

Given the leading role of the US in global LNG exports and of the EU in global LNG imports, the EU–US trade deal could, in principle, influence the global LNG market. However, considering the factors outlined above, the deal is more likely to function as a political signal of transatlantic solidarity than as a major commercial driver of energy trade growth, particularly in LNG. With EU gas demand structurally declining and climate targets accelerating the shift away from fossil fuels, long-term EU reliance on US LNG is neither economically nor environmentally sustainable. In a likely scenario, the EU–US trade deal may follow the trajectory of the 2019 US–China trade deal, which included commitments for China to increase imports of US energy products, including LNG. However, those targets were largely unmet because the provisions were non-binding, and actual imports were shaped by competition from other suppliers, logistical constraints, pricing fluctuations, and demand uncertainty, leaving US energy exporters with only modest gains.

Moreover, roughly 250 Mtpa of LNG export capacity is under construction worldwide, and overall supply is expected to grow in line with rising global gas demand under stable prices. This expansion provides sufficient room for all major LNG suppliers. With Asia driving the bulk of future LNG import growth, any additional US LNG directed to the EU is likely to be offset by increased supplies to Asia from other producers, primarily GECF member countries, thereby maintaining overall market equilibrium.