The outbreak of the coronavirus, which was followed by the implementation of various lockdown measures, resulted in a slowdown of economic activity in Japan during the first 10 months of 2020. Energy consumption dropped in the country due to lower demand in the service and industrial sectors, and consequently, LNG demand was affected in the aftermath of the COVID-19 pandemic. Overall, Japan's LNG demand fell by 4.7% (-3 mt) in the period January-October 2020, when compared with the same period last year.

The trend of LNG demand in Japan

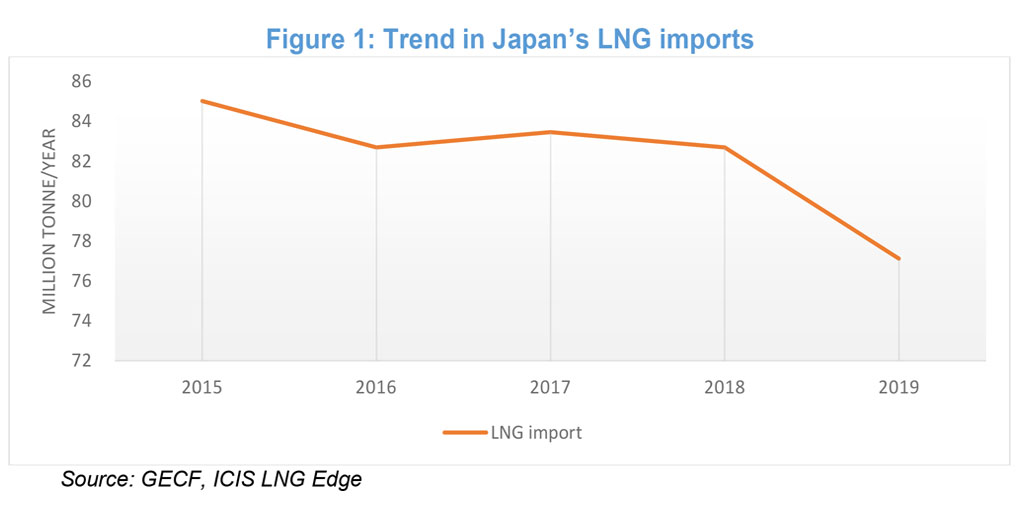

LNG demand in Japan, the biggest LNG importer in the world, has been declining over the past four years, falling from 85 million tonnes (mt) in 2015 to 77 mt in 2019. Warmer-than-average weather in recent years has resulted in lower LNG demand for seasonal heating in the residential and commercial sectors. Moreover, the slowdown in economic activity, coupled with lower industrial production and subdued external demand, have curbed LNG demand growth in the industrial sector. Further, the restarting of nuclear reactors and increasing nuclear power generation in recent years have led to a substantial reduction in gas demand for power generation. In 2019, Japan’s LNG imports stood at 77.2 mt, the lowest level since 2011. In summary, the resumption of nuclear power generation, mild weather pattern, high storage levels, and a slowdown in industrial activity during 2019 resulted in lower LNG demand as can be seen in Figure 1.

Whilst Japan has kept its position as the biggest LNG importer in Asia, its market share declined from 48% in 2015 to approximately 31% of the Asian LNG trade last year. In 2019, Japan imported LNG mainly from 12 countries, including Australia, Brunei, Indonesia, Malaysia, Nigeria, Oman, Papua New Guinea, Peru, Qatar, Russia, the UAE and the U.S. Australia held the largest share of LNG exports (39%) to Japan, followed by Malaysia (12%) and Qatar (11%).

Meanwhile, during the past couple of years, Japan's LNG imports from Australia and the U.S. have increased, replacing cargoes from the UAE, Malaysia and Qatar. The share of GECF Member Countries in Japan's LNG imports in 2019 stood at 41%, down from 47% a year prior. Within the GECF countries, Malaysia, Nigeria, Oman, Qatar, Russia, and the UAE are amongst the main LNG exporters to Japan.

Impact of COVID-19 on Japan’s economy

Since late January 2020, when the outbreak of the coronavirus started in Japan, economic activity has slowed in East Asia’s second largest economy. The first cases of coronavirus (COVID-19) in Japan were confirmed in mid-January 2020. The spread of the virus has been increasing since then with the number of confirmed cases exceeding 150,000 in the first week of December 2020. In the past 10 months, Japan has experienced two peaks of confirmed daily cases: on 12th April 2020 with a caseload of 743 and on 3rd August 2020 with 1,998 new infections. However, the rate of coronavirus mortality in Japan has been adequately controlled thanks to the country's strong healthcare system, an accepting culture of social distancing, well-equipped hospitals, as well as government support.

To contain the outbreak, the Japanese government announced several measures including social distancing, closure of schools, postponement of the 2020 Olympics as well as the partial shutdown of the service and industry sectors. It further declared a regional-level state of emergency on 7th April 2020 followed by a nationwide state of emergency a week later on 16th April 2020.

The implementation of strict lockdown measures and the state of emergency resulted in a slowdown of economic activity in the service and industrial sectors. However, the Japanese authorities announced fiscal and monetary packages to support the economy and to safeguard the health of the people. The government announced two emergency response packages to support economic activity. However, despite the significant policy stimulus by the authorities, Japan's economy experienced a significant contraction in the first half of 2020. According to the OECD, Japan’s economy declined by 0.6% in the 1st quarter of 2020, followed by a major downturn in the 2nd quarter. The country’s GDP shrank by 7.8% in the 2nd quarter of 2020 due to the lockdown and state of emergency in the months of April and May 2020. The economy is projected to decline by 5.3% in 2020 before turning around and growing by 2.3% in 2021, according to the IMF World Economic Outlook released in October 2020.

Impact of COVID-19 on Japan’s LNG demand

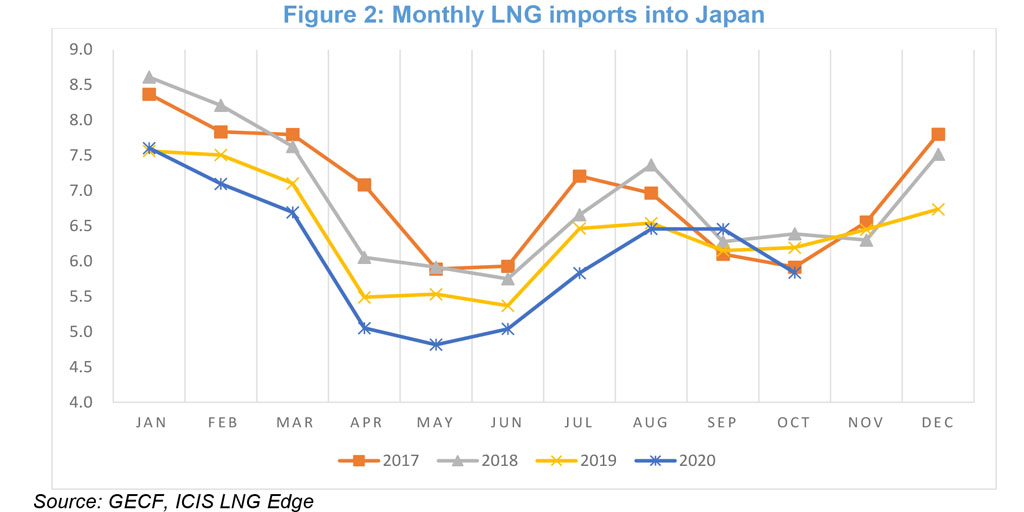

The slowdown in economic activity, combined with higher storage levels, meant Japan's LNG demand fell by 4.7% (-3 mt) in the period January-October 2020, when compared with the same period last year. In January 2020, Japan imported 7.6 mt of LNG, which is comparable to January 2019. LNG imports, however, began to fall in February 2020 onwards, with volumes reported at 7.1 mt in February, 6.7 mt in March, and 5.0 mt in April 2020.

In May 2020, Japan's LNG imports fell to 4.8 mt, its lowest level in the past decade. However, LNG imports have rebounded since June 2020 thanks to the lifting of the state of emergency, easing lockdown measures, and a rebound in economic activity. In June 2020, LNG imports into Japan climbed to 5.0 mt and rose to 5.8 mt in July 2020. Japan imported 6.5 mt of LNG in August 2020, almost the same level as in August 2019. Warmer-than-normal weather boosted gas demand for electricity and cooling in August 2020, compensating for the negative impact of COVID-19 on LNG demand in the country.

LNG imports in September 2020 stood at 6.5 mt, representing a 5% growth when compared with the same month last year, and supported by the recovery in the service and industrial sectors as well as stock building. Nevertheless, in October 2020, LNG imports fell again to 5.8 mt, a 5.7% y-o-y decline, due to lower power demand and cooler temperatures. Figure 2 shows the trend in Japan’s annual recent LNG imports on a monthly basis.

Although LNG imports have followed the usual seasonal pattern over the last 10 months, the negative effects of the pandemic combined with higher storage levels have resulted in a slowdown in LNG imports in 2020 as compared with the previous year. Japan imported 60.9 mt of LNG from January to October 2020, representing a 4.7% decline (or -3 mt) compared with the same period last year.

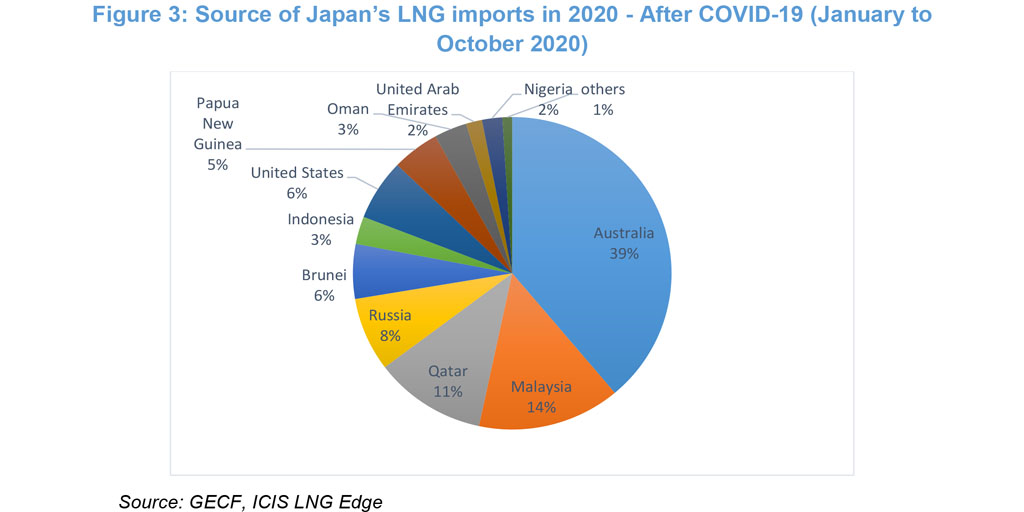

In terms of the source of Japan’s LNG imports in the first 10 months of 2020, the share of GECF countries slightly increased to 42% as compared with 2019. Among the GECF countries, Malaysia (+2%) and Nigeria (+1%) gained market share, while Oman and the UAE lost 1% of their market shares. Australia (39%), Qatar (11%), and Russia (8%) remained the main LNG import sources for Japan in 2020. Among non-GECF countries, the share of the U.S. LNG exports to Japan increased from 5% in 2019 to 6% in 2020.

Despite growing seasonal LNG demand during June-August 2020 because of higher-than-average temperatures this summer, a full recovery in Japan's LNG demand is not expected to take place in 2020. Higher storage levels and a weaker than expected gas demand recovery in the industrial and manufacturing sectors are expected to weigh on the LNG demand recovery over the remainder of 2020. Therefore, it is projected that Japan's LNG imports in 2020 will stay almost 4.5- 5% below the 2019 level.

Given the positive effects on LNG demand of economically driven coal-to-gas switching, compensated by the negative effects of nuclear power generation and higher storage levels, we could assume that the 4.5% decline in LNG demand over the past 10 months is mainly a result of the COVID-19 pandemic.

Although the restarting of nuclear reactors in Japan could weigh on LNG demand in the country, a recent court ruling to revoke the regulatory approval for the operation of some nuclear reactors could support an increase in LNG demand. At the beginning of December 2020, the Osaka district court in Japan ordered the government to revoke the approval granted for the operation of the Ohi 3 (1.18) GW and Ohi 4 (1.18 GW) reactors due to safety concerns expressed by residents. If similar rulings are handed down by local courts for other reactors, LNG and renewables would have to compensate for lower nuclear power, which would maintain the key role that LNG plays in Japan’s electricity mix.

References

1. Argus. (2020). Japan energy supply and demand report.

2. Enerdata. (2020). Japan country energy report, available at Enerdata database: https://www.enerdata.net/services.html

3. GECF Secretariat. (2020). Monthly Gas Market Report (MGMR) series

4. GECF Secretariat. (2020). Special Report: The Impact of COVID-19 on Natural Gas Markets, A Short Term Perspective.

5. ICIS LNG Edge Database

6. IGU. (2020). World LNG Report, available at https://www.igu.org/publication/302507

7. OECD. (2020). Unprecedented fall in OECD GDP by 9.8% in Q2 2020, available at https://www.oecd.org/sdd/na/gdp-growth-second-quarter-2020-oecd.htm

8. S&P Platts. (2020). Analysis: Japan's LNG demand unlikely to recover fully from COVID-19 in H2, available at https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/061220-analysis-japans-lng-demand-unlikely-to-recover-fully-from-covid-19-in-h2

9. World Health Organization (WHO). (2020). WHO Coronavirus Disease (COVID-19) Dashboard- Japan, https://covid19.who.int/

10. International Monetary Fund (IMF). (2020). World Economic Outlook, October 2020.

Dr Kamran Niki Oskoui

Market Research Analyst

Gas Market Analysis Department