The GECF Annual Statistical Bulletin 2024 showcases the significant impact of GECF Countries on the global natural gas sector, emphasizing key achievements and trends through 2023. This summary offers an overview of their contributions to reserves, production, trade, infrastructure, and economic resilience.

1.1. GECF: A Leader in Global Natural Gas

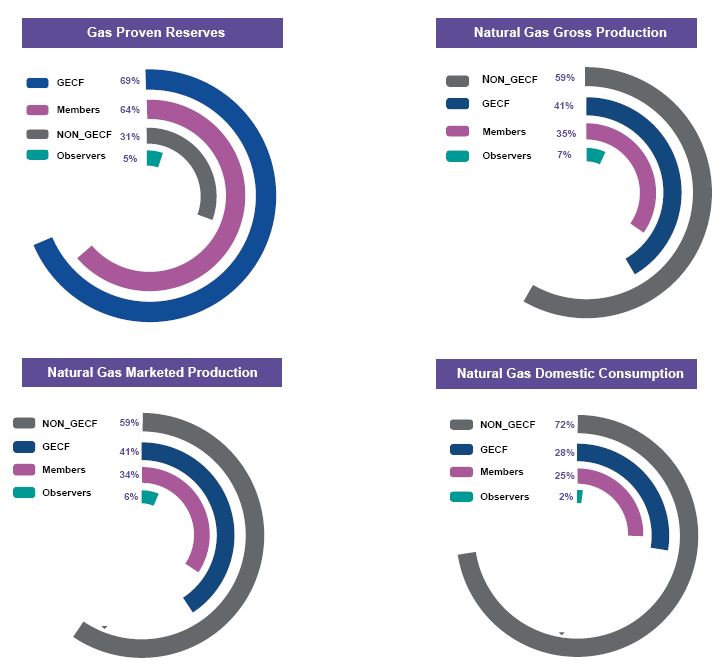

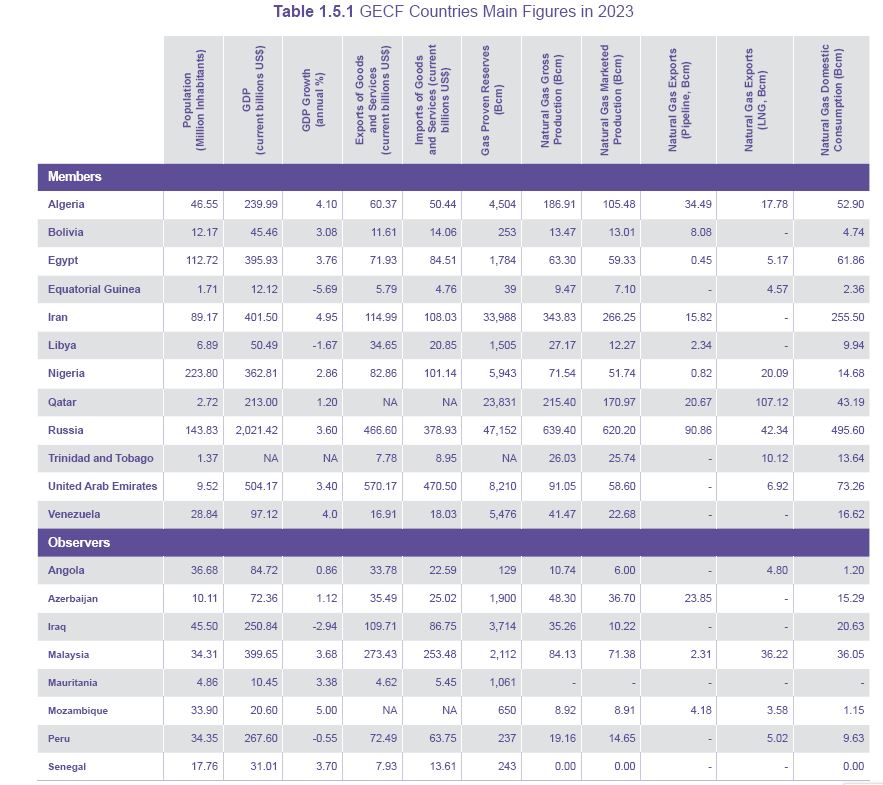

In 2023, GECF countries continued to demonstrate their dominance in the natural gas sector, holding more than 69% of the world’s proven reserves, equivalent to almost 145,000 Bcm. This unrivalled share underscores the long-term resource security offered by GECF Countries, led by major reserve holders like Russia, Iran, and Qatar. Collectively,

GECF countries contributed 41% of global marketed production, solidifying their role as reliable suppliers to meet global energy demand. In the realm of consumption, GECF Countries represent 28% of global domestic consumption.

1.2. Key Contributions in Global / Regional Trade

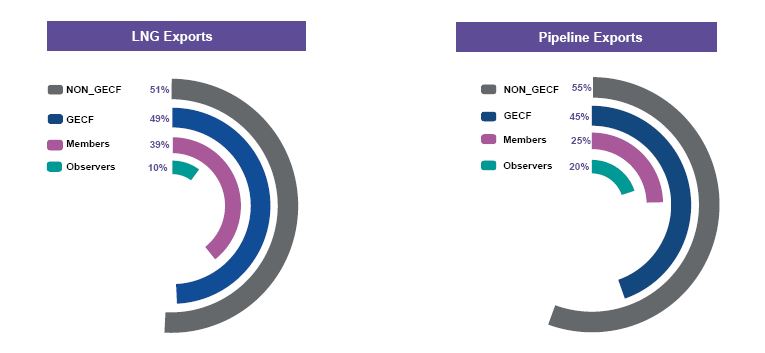

The lower consumption share, relative to production (28%), highlights GECF’s significant role as net exporters in the natural gas markets. GECF’s influence is particularly pronounced in exports, where they hold 49% and 45% shares of the LNG and pipeline exports respectively. GECF countries retained their position as leaders in LNG trade, accounting for more than 49% of global LNG exports. Qatar remained the top LNG exporter more than 107 Bcm, catering to growing demand in Asia and Europe.

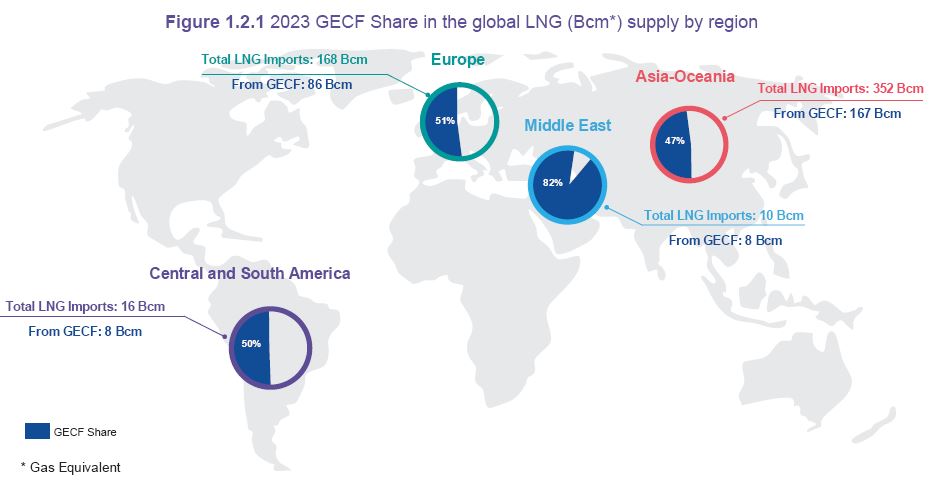

- Asia’s LNG demand rebounded to 352 Bcm, with 47% (167 Bcm) supplied by GECF Countries.

- Europe increased its LNG imports to 168 Bcm, with 51% (86 Bcm) coming from GECF Countries to enhance energy security.

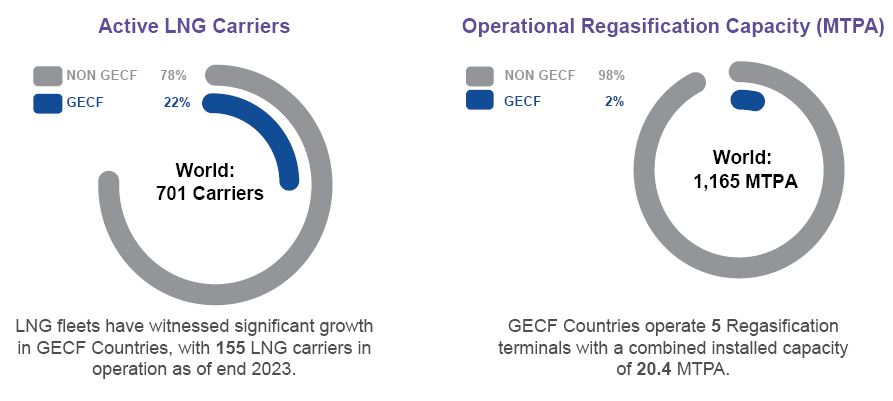

- Africa emerged as a key supplier, with countries leveraging their resources to meet global demand like Algeria, Nigeria, and Mozambique which achieved a milestone by entering the LNG market, signalling its growing role in global energy trade and further diversified GECF Countries LNG portfolio, while expanded liquefaction capacity (up to 241 MTPA) and a fleet of 155 LNG carriers ensured seamless delivery to global markets.

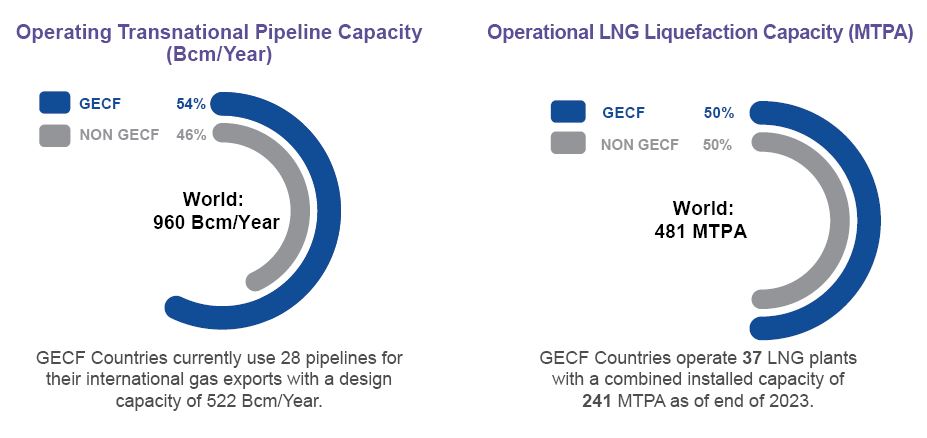

1.3. Infrastructure Strength and Global Impact

In 2023, GECF Countries reinforced their global position through significant investments in natural gas infrastructure operating 37 liquefaction plants (70 Trains) with a combined capacity of over 241 MTPA, ensuring reliability and scalability in LNG exports. The pipeline network, spanning thousands of kilometres, remained a critical component for regional and crossborder gas transportation. GECF Countries continued to optimize their pipeline systems to meet changing trade flows, particularly considering shifting energy policies and geopolitical pressures. Notable contributors to pipeline stability include Algeria, which sustained exports to Europe, and Russia, which maintains one of the largest pipeline infrastructures globally.

LNG shipping logistics further enhanced GECF’s competitive edge. Member countries collectively operated a fleet of 155 LNG carriers, capable of transporting large volumes across long distances. These carriers ensured the flexibility and accessibility of natural gas, making LNG a cornerstone of the global energy transition.

The combined strength of liquefaction plants, pipelines and LNG fleets showcases GECF’s commitment to delivering reliable and efficient natural gas supplies, maintaining its position as a leader in the global energy market.

1.4. Gas Market Prices and Stabilization

In 2023, global natural gas markets experienced welcome stabilization following the extreme price volatility of 2022. This year marked a return to the relative balance between supply and demand, as energy markets adapted to geopolitical shifts and infrastructure developments. Key benchmarks reflected this shift, with Henry Hub prices averaging $3.50/MMBtu, a substantial decline from the elevated levels of 2022, driven by strong U.S. production and steady exports. In Europe, TTF prices settled at an average of $15/MMBtu, significantly lower than the spikes of the previous year. This adjustment was underpinned by robust LNG supply chains, increased storage levels, and

diversification efforts across European importers. The stabilization of gas prices in 2023 underscores the adaptability of GECF countries in responding to market needs. By leveraging their robust production and export infrastructure, particularly in LNG, GECF nations played a central role in rebalancing global gas markets. Shipping costs for LNG also normalized, easing logistical pressures that had amplified market disruptions in 2022. The global LNG fleet, including GECF member-operated carriers, played a pivotal role in facilitating smoother trade flows. These developments ensured the continued delivery of LNG to key regions, particularly Europe and Asia, where demand remained strong.

1.5. Economic Resilience and Rising Domestic Demand

The population of GECF Member Countries reached approximately 900 million in 2023, this significant population base fueled a steady rise in domestic energy demand and supported the expansion of a robust labor force essential for industrial growth and economic diversification. Across Member Countries, natural gas played a vital role in meeting

these growing energy needs, with domestic gas consumption rising by 2.8%, reaching a total of 1042 Bcm. This increase reflects enhanced access to energy and sustained economic growth, particularly in countries such as Iran, Egypt, and Nigeria, where industrialization and urbanization have driven higher gas demand. The economic stability of GECF Countries remained closely tied to their natural gas sectors, which continued to act as a cornerstone of their national economies. Countries like Qatar and the UAE demonstrated robust GDP growth, underpinned by revenues from LNG exports and strong global demand for reliable energy supplies. Trade balances were buoyed by these exports, which played a pivotal role in regions like Europe. For example, Algeria emerged as key exporters to Europe, leveraging their proximity and infrastructure to capitalize on shifting trade dynamics.

The power generation sector remained the largest consumer of natural gas, accounting for 45% of total domestic consumption, followed by residential demand at 30%. Countries like Russia, Iran, and Nigeria led this growth, with Russia increasing its domestic consumption by 9.18 Bcm and Iran adding 6.36 Bcm, driven by expanding industrial demand and urban population growth. Nigeria’s domestic consumption rose by a notable 13.2% (+1.71 Bcm), reflecting its push toward greater utilization of natural gas in transportation and economic development. The economic and demographic dynamics of GECF Countries highlight their ability to balance growing domestic demand with international export commitments. By prioritizing investments in infrastructure and energy distribution networks, GECF member countries are ensuring reliable and affordable energy for their populations while maintaining their position as global leaders in natural gas markets.

1.6. Navigating Change: GECF Members’ Performance in 2023

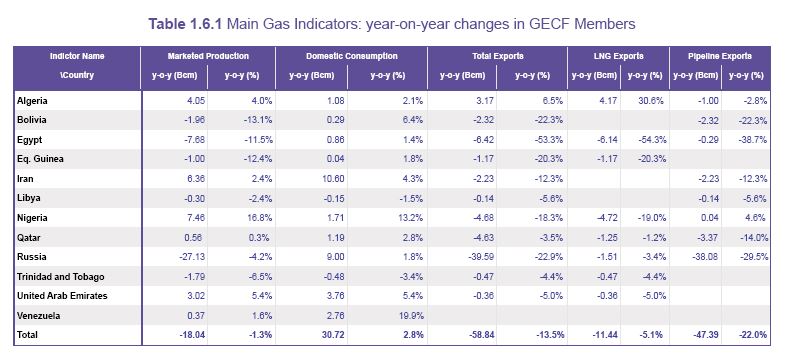

Marketed production across GECF Members experienced a decline of 18.65 Bcm, representing a 1.3% drop compared to the previous year. In contrast, several Member Countries demonstrated robust growth, with Nigeria achieving the highest increase at 7.46 Bcm, representing a remarkable 16.8% growth. Other contributors included Algeria, which

increased production by 4.05 Bcm (4.0% growth), and the United Arab Emirates, which added 3.02 Bcm for a 5.4% y-o-y growth rate. These increases reflect these countries’ capacity to sustain output despite market challenges.

Domestic consumption across GECF Countries rose by 28.79 Bcm, an increase of 2.8%, marking the 3rd consecutive year of growth. This rise highlights the growing importance of natural gas for power generation and residential use across countries. Russia led in domestic consumption increases, adding 9.18 Bcm, followed by Iran, which saw a rise of 6.36 Bcm (2.4% growth) as it continued to expand its use of natural gas for industrial and residential utilization. Nigeria also showed strong growth, with consumption increasing by 13.2%, reflecting its efforts to integrate gas more deeply into its energy mix.

1.7. Progress in Reducing Gas Flaring in 2023

In 2023, GECF Countries made significant strides in reducing gas flaring, contributing to lower greenhouse gas emissions and improved resource efficiency. In Africa, Algeria achieved a slight reduction, cutting flaring by 0.4 Bcm, representing a 5% decrease and reflecting its commitment to efficient gas usage and sustainable energy practices.

Nigeria reduced gas flaring by 4%, bringing levels down to 5.10 Bcm, showcasing consistent efforts to lower emissions. In South America, Trinidad and Tobago stood out with a remarkable 33% decrease, lowering flaring to 0.06 Bcm. Bolivia achieved a 30% reduction, cutting flaring to 0.09 Bcm, signalling significant progress despite smaller initial

volumes. Peru cut gas flaring by 8%, bringing levels down to 0.11 Bcm. Venezuela made substantial progress, reducing flaring by 18% to 14.31 Bcm, a step forward in its commitment to improved gas management. In the Middle East, Iraq registered a 2% reduction, lowering flaring levels to 15.85 Bcm, reflecting incremental improvements in environmental performance. In Southeast Asia, Malaysia recorded a 12% decrease, reducing flaring to 0.90 Bcm. In Eurasia, Russia achieved significant reductions, cutting flaring by 23%. This marked a notable advancement in its environmental practices. Altogether, these efforts resulted in a total reduction of 50.79 Bcm in gas flaring for 2023. These achievements highlight the global momentum toward sustainable energy practices and reducing the environmental impacts of gas flaring.

1.8. 2023 in Focus: A Milestone Year in GECF’s Decade of Energy Leadership

The year 2023 demonstrated the remarkable resilience, adaptability, and leadership of GECF Countries, even amid global energy market fluctuations. GECF Countries collectively maintained their crucial role in global energy security by balancing domestic needs with international trade, advancing infrastructure investments, and supporting a steady growth trajectory for natural gas. Gross production of natural gas across GECF Countries remained robust in 2023, reaching approximately 2,068 Bcm. While marketed production experienced a slight decline of 1.6%, this stability reflects the capacity of GECF Countries to adapt to evolving global demand, with increased contributions from countries like Algeria, Nigeria, and Iran offsetting reductions elsewhere.

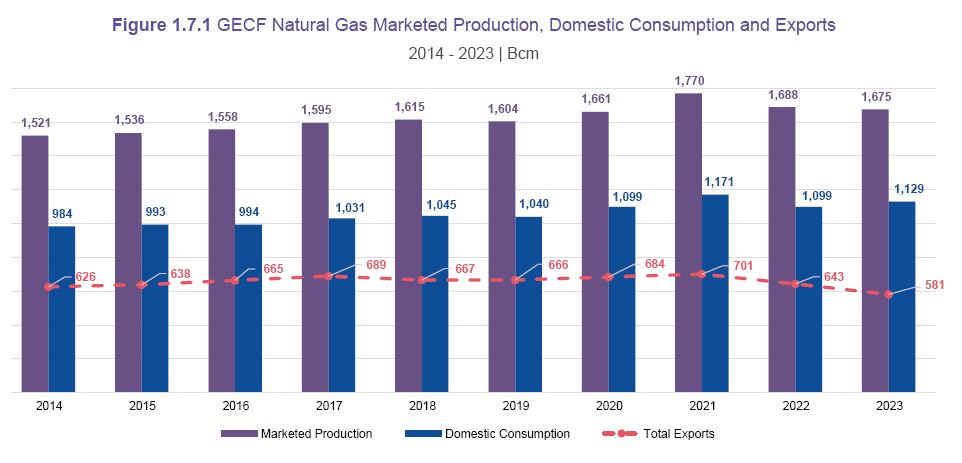

Domestic consumption reached a decade-high of 1,129 Bcm, continuing its upward trend as natural gas remained a key energy source for power generation and residential needs. This growth underscores GECF Countries’ commitment to meeting their populations’ rising energy demands while supporting economic growth and industrial expansion. At the same time, GECF Countries contributed 581 Bcm to global natural gas exports, reaffirming their role as reliable suppliers to international markets. As demand for cleaner, more reliable energy sources continue to grow, the achievements of 2023 position GECF Countries as indispensable players in driving the transition to a more sustainable global energy system. With a stable foundation in production, consumption, and trade, GECF Countries are well-prepared to meet the opportunities and challenges of the years to come.