Gas storage is an integral facet of the supply-demand balance of gas markets, underpinning supply during peak consumption periods and providing flexibility. This is particularly significant for the gas markets of the European Union (EU), which have long relied on underground gas storage as an extra source of supply during the winter season to meet the higher heating demand. As such, the EU has an established cycle of restocking of gas storage sites during summer months (characterized by lower gas demand), in anticipation of net gas withdrawals in winter months when gas demand almost doubles.

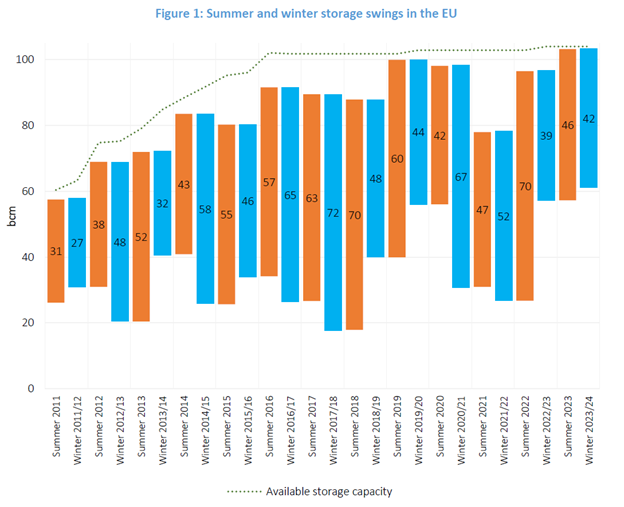

Over the years, there has been an increase in the total working capacity of underground gas storage in the EU, reaching 104 bcm by 2022, which has facilitated ever increasing swings in storage levels over the seasons. The chart below shows the range of net gas injections in the summer season and withdrawals in the winter season, as well as the level of gas in storage at the start and the end of each summer and winter season, displayed in orange and blue, respectively (Figure 1). The summer season covers the period from April to October, while the winter season encompasses the period from November to the succeeding March.

Source: GECF Secretariat based on data from AGSI+

Until the start of the 2019/20 winter season, the level of gas in storage rarely approached the maximum available, with the EU countries filling storage sites to an average of around 90% of the capacity up to this period. However, during four out of five latest winter seasons, gas storage sites have been filled much higher than the average level, closer to the maximum available, with the exception of 2021/22 winter season.

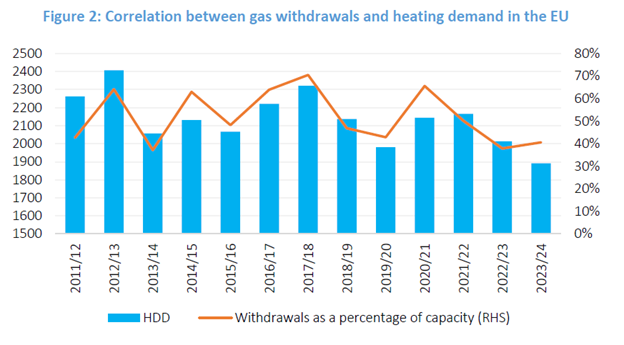

Examining the data more closely reveals the trend between the winter gas withdrawal volumes and temperature in the EU (Figure 2). Heating degree days (HDDs) are a measure of the relative difference between the mean daily temperature and a reference temperature, and therefore have an impact on the heating demand of the region. There is a general correlation between the two variables, as illustrated by the level of gas withdrawals as a percentage of the total gas storage capacity for each particular season. The higher HDD number in a specific winter season usually corresponds to higher gas withdrawals. In addition, there are also other factors which influence the quantity of winter gas withdrawals, such as the availability of ample gas supply, from either domestic production or imports whether that be pipeline gas or LNG.

Source: GECF Secretariat based on data from AGSI+, Eurostat and LSEG

The winter seasons of 2012/13 and 2017/18 were notable for a relatively large percentage of gas withdrawal from storage, driven by a high HDD number for those periods. Also, the winter seasons 2014/15 and 2020/21 demonstrated higher-than-average withdrawals compared with relatively low HDD numbers, mainly due to economic rationale. For instance, in the winter season 2020/21, the European market operators prioritized an extensive withdrawal of gas, which had previously been injected into the storage facilities at the record low prices in the summer of 2020, amidst the Covid-19 pandemic. In addition, at that time, the market witnessed a fast recovery in LNG demand in Asia, with LNG suppliers preferring Asia as a destination for LNG cargoes. As a result, the withdrawn gas was extensively used for consumption at that time, while spot and long-term contract LNG purchases dropped. Where there were milder-than-average winter seasons, such as the 2019/20 and 2022/23, there was a much lower quantity of gas required to be taken from storage.

Gas storage developments contributed significantly to the European energy crisis in 2022. The region entered the 2021/2022 winter season with only 76% of gas storage capacity filled and ended that season with only 26% capacity filled, both figures being historical lows from the last decade. With low storage levels and a sharp decline in pipeline gas imports to the region amidst the geopolitical developments, the EU found itself in a significant deficit of gas supply. To avoid the escalation of the crisis during the subsequent winter season, the EU authorities introduced new legislation to keep gas in storage at sustainable levels.

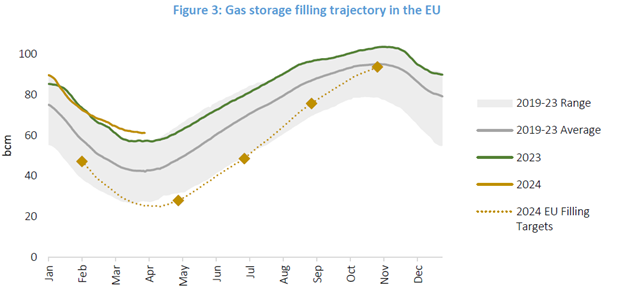

In June 2022, the European Commission presented a regulation on targets for gas storage to be reached in anticipation of the forthcoming winter season. Those filling regulations mandate that EU countries should fill gas storage sites to a minimum of 90% capacity by November 1 each year, regardless of the price of gas, to guarantee security of gas supply in winter seasons. In addition, in November 2023, the European Commission introduced a regulation, which set the filling trajectory with intermediary targets for 2024 for each member state (Figure 3). Together with successive warm winters, the legislation implemented by the European Commission has been influential in mitigating the risk of gas shortfall during the recent previous two winters.

Source: GECF Secretariat based on data from AGSI+ and the European Commission

The winter season of 2023/24 started with 99% of capacity filled. According to the legislation, the first checkpoint for 2024 was February 1, at which point the EU collectively had 25 bcm more gas in storage than the Commission’s target. During the full winter season, only 42 bcm were withdrawn, which was the second lowest indicator over the last decade. That happened amidst the lower heating demand caused by the warmest winter for over the last 12 years.

The low withdrawals resulted in gas storage reaching 61 bcm at the end of the winter season, which is the highest ever level for winter season end. This creates favourable conditions for the European market in preparation for the 2024/25 winter season, since the gas storage will be close to the maximum capacity with only 40 bcm of net gas injection required in the upcoming summer season. Such low injection requirements are expected to contribute to enhancing stability on the regional and global gas markets, while exerting downward pressure on spot prices.