The United Nations Conference on Trade and Development (UNCTAD) has estimated that the maritime sector accounts for 3% of global greenhouse gas (GHG) emissions, representing over 1.5 Gt of CO2 (carbon dioxide) per year equivalent. The emissions from this particular sector have grown by some 20% over the last decade, underpinned by the rising levels of shipping activities, related mainly to global maritime trade.

The EU is one of the key players in the global maritime industry. However, unlike the power, manufacturing and aviation sectors, the maritime industry was not covered, until recently, by the EU Emissions Trading System (EU ETS). The EU ETS, established in 2005, functions in all 27 EU member states plus Iceland, Liechtenstein and Norway, covering around 45% of the EU’s GHG emissions. The EU ETS operates on the basis of a ‘cap and trade’ principle, in which a cap is set for the total GHG emissions that can be emitted within the system. Participants are allowed to trade their EUAs (European Union Allowances) based on their needs, but they must have sufficient allowances to cover their total emissions for each year, or else they will be subject to heavy penalties. In this way, the EU ETS provides financial incentives to cut emissions, while also promoting investment in low-carbon technologies. Importantly, as the cap is reduced over time, overall emissions are also lowered.

On 18 April 2023, the European Parliament formally adopted the “Fit for 55” package, which aims to raise the 2030 emissions reduction target to 55% (compared to 1990 levels) in its drive towards carbon neutrality by 2050. The package includes a combination of initiatives such as extending the EU ETS to new sectors, as well as tightening the existing EU ETS, increasing the role of renewables, improving energy efficiency, accelerating zero-emission and low-carbon fuels in transportation, and preventing carbon leakage.

In particular, the EU ETS has been extended to the maritime industry, which accounts for 0.14 Gt of CO2 annual emissions out of total regional emissions of 2.3 Gt. The EU ETS covers CO2 emissions from all large ships entering EU ports, effective from January 2024. Large ships are defined as those with a gross tonnage of 5,000 and above, which are considered to be responsible for 85% of total CO2 emissions from the maritime sector.

According to the new regulation, shipping companies are required to report emissions data as stipulated under the Monitoring and Reporting Verification (MRV) Regulation, through a platform operated by the European Maritime Safety Agency (EMSA). On an annual basis, companies must submit an emissions report for each ship under their responsibility, as well an aggregated emissions report at company level. For instance, data for 2024 must be verified by an accredited verifier by 31 March 2025. Once verified, companies must provide the equivalent number of EUAs to the administering authorities of the EU Member States by 30 September 2025.

To ensure a smooth implementation of the new regulation, shipping companies are obligated to cover only a portion of their emissions during an initial phase-in period as follows:

- For 2025: 40% of their emissions in 2024;

- For 2026: 70% of their emissions in 2025;

- For 2027 onwards: 100% of their emissions in the previous year.

Furthermore, the system will be flag-neutral and route-based, covering the following voyages:

50% of emissions from voyages either starting or ending outside of the EU;

100% of emissions that occur between two EU ports and when ships are within EU ports.

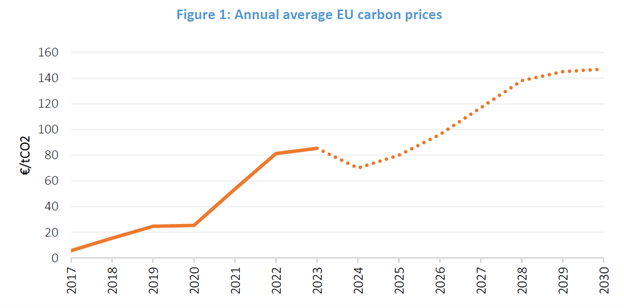

In order to cover their emissions, shipping companies need to have sufficient EUAs, which are based on the EU carbon prices. Since 2017, EU carbon prices have been steadily increasing. Moreover, they are expected to continue to increase until 2030, with the exception of 2024 (Figure 1). In 2023, the EU carbon price averaged €85/tCO2, reflecting a 5% increase y-o-y. Moreover, the daily EU carbon price reached a record high of €100/tCO2 at the end of February 2023, propelled by strong buying interest from utilities and low wind generation. However, in 2024, the EU carbon price is projected to decrease, with an annual average of €70/tCO2, according to estimates from Refinitiv Eikon (as of April 17, 2024). This forecast was adjusted downward following a bearish Q4 2023, which was closely associated with weak gas market fundamentals. Additionally, expected lower industrial demand, stemming from sluggish economic growth, is likely to further impact the demand for EUAs in 2024. Furthermore, in the medium/long-term, the cost of EUAs is expected to gradually increase, reaching slightly above €145/tCO2 by 2030.

Source: GECF Secretariat based on data from Refinitiv Eikon

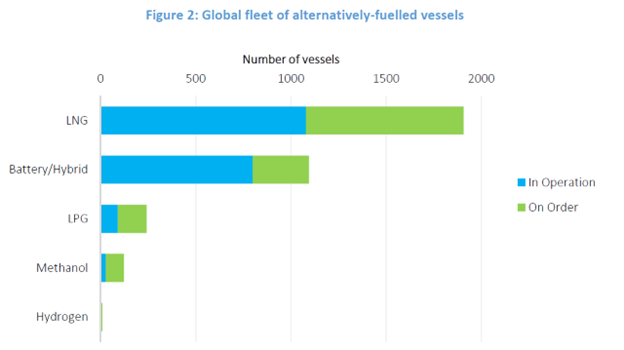

Currently, the main source of propulsion for the maritime sector are fuel oils, typically heavy fuel oil (HFO). HFO has been the preferred ship fuel due to its high energy density, as well as its relatively low cost, compared to other lighter ends derived from the crude oil refining process. However, the continued use of HFO has come under scrutiny with respect to its negative impact on the environment, specifically through the emissions of CO2, as well as particulates and other harmful compounds. In this context, the maritime industry is introducing alternative fuels, which account for 2% of the world’s shipping fuels consumption. In particular, LNG bunker fuel is gaining momentum, with almost 1,100 LNG-fuelled vessels in operation, accounting for circa half of the alternatively-fuelled fleet (Figure 2).

Source: GECF Secretariat based on data from DNV

By including the maritime industry in the EU ETS, the regional authorities seek to economically incentivise a shift away from traditional polluting maritime fuels to alternative fuels. In this context, the new regulation may become an additional driver to the structural shift towards LNG bunker fuel in the maritime sector, complementing other global-level regulations established by the IMO.

An expected consequence of the new regulation is that the EU carbon cost may rise, with the EUAs contributing to the total cost of maritime transportation, especially when the regulation is fully ramped up. In this context, the usage of LNG bunker fuel will result in lower carbon cost compared to HFO, since the combustion of LNG reduces CO2 emissions by at least 20%.

The experience of the EU in including the shipping sector into the ETS may prove to be a blueprint for other regions, since the EU ETS is the world’s oldest and largest international emissions trading system. For example, China established a national ETS, which currently does not cover its shipping industry. In the meantime, at the provincial level, local markets such as the Shanghai ETS has covered the maritime sector since 2021, which may be expanded country-wide in future, and may have a positive impact on LNG bunker fuel consumption.

The long-term viability for LNG bunker fuel is evidenced by the growing share of LNG-fuelled vessels in the global orderbook of newbuild ships, as well as the continued development of LNG bunkering infrastructure. According to the GECF Global Gas Outlook 2050, gas demand in the maritime industry will expand sharply to 90 bcma by 2050. In this context, it is important to highlight that at the 7th GECF Summit, held on March 2, 2024, Heads of State and Government of GECF Member Countries adopted the Algiers Declaration, in which they reaffirmed the commitment to “foster the increased use of natural gas in maritime and land transportation, and develop necessary infrastructure to provide it efficiently and cost-effectively to all consumers.”