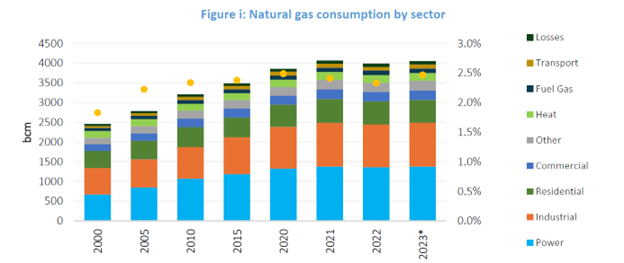

While the power generation, industrial and residential/commercial sectors have retained their high shares in global gas consumption over the past two decades, the transport sector is still regarded as an emerging industry for gas utilisation. Since the year 2000, the share of the transport sector in global gas consumption has expanded from around 1.8% to an estimated 2.5% in 2023 (Figure i). This sector consumes around 100 bcm per annum, and this is projected to rise consistently in the medium and long term. In the meantime, according to Enerdata, the transport sector is dominated by the utilisation of oil-based fuels, accounting for 92% on the global level in 2023, while the remaining part belongs to alternative fuels, including natural gas, whose share rose to 2.5% compared to 0.4% in 2000.

Source: GECF Secretariat based on data from Rystad; Data with the asterisk (*) is estimated

Source: GECF Secretariat based on data from Rystad; Data with the asterisk (*) is estimated

The transport sector is poised to expand its share of global gas consumption, particularly through the increase in uptake from the road transport segment of the market, driven by two complementary factors, namely favourable energy policies and economic competitiveness.

The environmentally focused energy policies have had an undeniable influence on the shifting fuel choices in the transport sector. The transport sector is responsible for one quarter of global greenhouse gas emissions, with road transport standing out with a lion share of emissions. Amidst the reinforcing climate change agenda, this may make the decarbonisation of the transport sector, particularly the road transport segment, an imperative.

One of the most efficient ways to promote the decarbonisation of road transport is switching from conventional oil-based fuels to natural gas. Compared with conventional fuels, switching to natural gas may reduce GHG emissions by around 20%, while carbon dioxide emissions in particular may decrease by up to 25%. In addition to these reductions, the combustion of natural gas-based fuels produces lower levels of nitrogen oxides, sulphur oxides and particulate matter, further contributing to improving air and water quality. In this context, the use of natural gas as a transport fuel has proven advantageous in advancing social progress and mitigating the effects of climate change, while contributing to meeting the United Nations’ Sustainable Development Goals (SDGs), particularly SDG 7 (Affordable and clean energy), SDG 11 (Sustainable cities and communities) and SDG 13 (Climate action).

In road transport, the fuels for natural gas vehicles (NGVs) are compressed natural gas (CNG) and liquefied natural gas (LNG). CNG systems, due to the requirement of a high-pressure storage tank, were initially limited to larger vehicles, but are now widespread in cars, rickshaws and motorcycles. The popularity of CNG is aided by the fact that the fuel is easy to adapt to the petrol-fuelled internal combustion engine, requiring just minor modifications to the fuel storage and intake systems. On the other hand, LNG has a much higher energy density, and is therefore only suitable for heavy hauling and long-range transportation; thus LNG-fuelled systems are increasingly deployed in buses, trucks, municipal utility vehicles, agriculture machinery, ships, including LNG carriers, and even in rail transport. With fuel mileage of these vehicles reaching 800 to 1000 km between refuelling, LNG systems are particularly suited for these applications. Moreover, liquid petroleum gas (LPG or autogas), which consists primarily of propane and butane, are also extracted as part of natural gas and/or oil production, and so may also fall into the category of natural gas fuels.

Currently, there are more than 30 million vehicles worldwide, which use either CNG or LNG fuelled systems, and nearly the same number of vehicles, which are powered by LPG.

Asia Pacific countries are continuing their rapid scale-up of natural gas vehicle programs. China is the global leader in terms of number of NGVs. In addition to the well-developed market of passenger vehicles, the domestic market of large buses and heavy-duty trucks has also gained momentum recently. Most notably, currently one in three new heavy-duty trucks sold in China runs on LNG. The government of India is also committed to expanding the uptake of NGVs, with the CNG vehicle sales recording strong double-digit annual growth to exceed 1 million units in 2024.

The EU countries are adopting several energy policies for the decarbonisation of the transport sector. Central to these is the Fit for 55 legislation, which targets a 55% reduction in emissions by 2030, compared with 1990 levels. One key tool of this is the EU’s Emissions Trading Scheme (ETS), which will include emissions from the road transport sector starting in 2027. In this context, the EU aims to expand the infrastructure for alternatively fuelled vehicles, including natural gas. Currently, there are over 4,200 CNG refuelling stations and over 740 LNG refuelling stations in Europe. As of July 2024, the European Alternative Fuels Observatory reported that there are 8.4 million vehicles which operate on LPG in the region, along with 1.5 million CNG vehicles and 9,400 LNG vehicles. In the meantime, recently adopted legislation creates both incentives and barriers for the penetration of NGVs. In April 2023, the EU adopted legislation on strengthening the CO2 emission performance standards for new passenger cars and new light commercial vehicles in line with the EU’s increased climate ambition. According to it, from 2035, all new cars coming on the market cannot emit any CO2. The next step is an adoption of a similar legislation on heavy-duty vehicles. The pending draft legislation would mandate manufacturers to cut the average emissions of new trucks by 45% in 2030 and 90% in 2040, which would phase out almost all sales of new diesel trucks. While putting NGVs, notably for lower emissions, in a more favourable position compared to gasoline and diesel vehicles, such measures however may also penalise NGVs, since these bans promote only zero or close to zero emission options. In this context, the global gas industry, facing these challenges, has additional incentives to advance the decarbonisation.

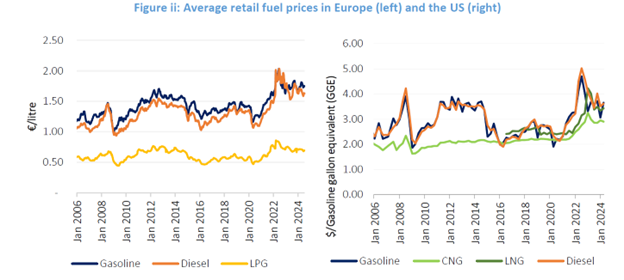

The second major driver for natural gas penetration in the road transport sector is the cost competitiveness of natural gas fuels. In particular, LPG fuel price has been lower than gasoline and diesel in Europe over the last two decades, while CNG and LNG fuels price has tended to be more competitive compared to oil-based fuels in the US most of the time over the same period (Figure ii). The major exception was the energy crisis in 2022, when global gas prices reached record highs, which undermined to a certain extent the competitiveness of NGVs. However, with the gas markets having entered into a phase of stability and lower prices afterwards, the market positions of NGVs have started reinforcing again.

Source: GECF Secretariat based on data from the European Commission and from US AFDC

Source: GECF Secretariat based on data from the European Commission and from US AFDC

Source: GECF Secretariat based on data from the European Commission and from US AFDC

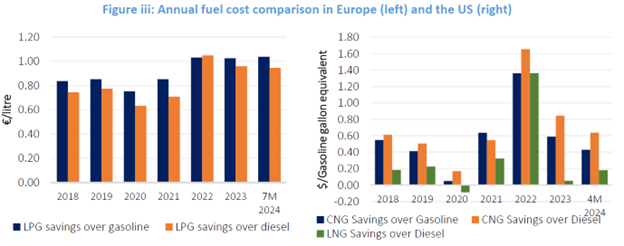

In the European market, the price of retailed LPG for NGVs has consistently been lower than gasoline or diesel, even factoring the relevant regional taxes and duties. As such, since 2018, LPG savings over gasoline averaged €0.91/l and LPG savings over diesel averaged €0.83/l (Figure iii). In the US, barring the outlier of 2022, since 2018, CNG savings over gasoline and diesel averaged $0.45/Gasoline Gallon Equivalents (GGE) and $0.55/GGE respectively, while LNG savings over diesel averaged $0.15/GGE. Moreover, this economic competitiveness is set to continue in the medium term, as the commissioning of huge new LNG export capacity in the upcoming years may put downward pressure on gas prices.

Source: GECF Secretariat based on data from the European Commission and US AFDC

Source: GECF Secretariat based on data from the European Commission and US AFDC

In this context, although the initial purchase cost of NGVs may be higher compared to vehicles running on conventional fuels due to the specialized equipment for fuel storage and injection, NGVs may be more cost-competitive than gasoline or diesel counterparts in the long run. This is due to lower fuel costs, longer ranges between refuelling, longer engine life, and lower maintenance costs resulting from the cleaner fuel.

In the meantime, the advancement of NGVs often requires governmental support, such as investing in gas transportation and NGV refuelling infrastructure or implementing favourable regulations such as providing tax incentives or subsidising natural gas fuels. Moreover, the emerging global trend towards decarbonisation of road transport may require an active participation of governments in promoting the decarbonisation of the gas industry.

The GECF Member Countries are among the global leaders in the adoption of NGVs while leading by example, with Iran in particular being second only to China on the global level with respect to gas consumption for road transport. Beyond the advantages of lower GHG emissions and fuel cost savings, gas producing and exporting countries, through expanding the usage of NGVs on local markets, also benefit from increasing domestic gas demand. Furthermore, gas suppliers, which invest in NGV infrastructure in external markets, may stake out reliable markets.

At the 7th GECF Summit held in March 2024 in Algeria, the Heads of State and Government of the GECF Member Countries resolved their common determination to “foster the increased use of natural gas in maritime and land transportation, and develop necessary infrastructure to provide it efficiently and cost-effectively to all consumers”. Additionally, on the sidelines of the summit, the GECF inaugurated the headquarters of its Gas Research Institute (GRI), which will serve as the platform for scientific and technological collaboration amongst the Member Countries, with a project on “LNG as a fuel in the transportation sector and in bunkering” selected as one of its first priority projects. Moreover, the GECF Secretariat continues to explore the potential for expanding natural gas usage in the transport sector, while organising specific events on this topic, with the workshop on natural gas utilization in the transport sector held in May 2023.