As a global economic powerhouse, the leading energy consumer, the biggest emitter of energy-related CO2, the topmost renewables producer and the largest hydrocarbon importer, China increasingly influences the global energy markets, including the gas markets.

The energy development of China is currently carried out in line with the 14th Five-Year Plan, covering the period of 2021-2025. The Plan is built on four main pillars addressing energy security, energy efficiency, energy transition and innovation, and translates into ambitious targets of 18% reduction in CO2 intensity and 13% reduction in energy intensity by 2025 compared to 2020 levels. Moreover, the Chinese natural gas industry is guided by the National Gas Utilisation Policy, initially adopted in 2007 and amended in 2012 and also 2024. Its latest edition, which came into force on 1 August 2024, is designed to regulate the utilisation of natural gas, optimize the consumption structure, and ensure a balanced supply-demand system by coordinating production, supply, storage, and sales. Additionally, it seeks to enhance the positive role of natural gas in advancing the development of a new energy system. According to the Policy document, the utilization of natural gas is divided into priority, permitted, restricted and prohibited categories. For priority gas use projects, local governments at all levels and relevant departments are encouraged to provide policy support in terms of planning, land use, financing, and taxation.

China is the global leader in primary energy consumption, holding a 27% share, which is equivalent to the combined share of the US and EU. Coal dominates China’s energy mix with a 62% share, while natural gas ranks third, contributing 9%.

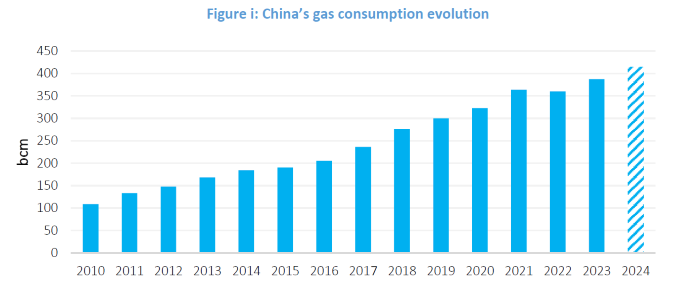

China became the third largest gas market in 2023, surpassing the EU and lagging behind only Russia and the US. Its gas consumption rose from 27 bcm in 2000 to 387 bcm in 2023, with the compounded annual growth rate reaching 12% over this period (Figure i). China’s gas consumption growth is underpinned by intensive infrastructure development. In 2023, the total length of transmission gas pipelines reached 124,000 kilometers, with key projects enhancing the connectivity and reliability of gas supply across the nation. Furthermore, underground gas storage has become an integral part of China’s gas market, with its working capacity standing at 21 bcm, and targeted to increase to 80 bcm by 2035.

Source: GECF Secretariat based on data from Cedigaz

From the sectoral perspective, the industrial sector is the leader in China’s gas consumption, with 160 bcma. The country’s industrial sector, highly represented by energy-intensive industries, accounts for 38% of the national GDP (compared to 25% in the EU and 18% in the US) and has final energy consumption two times higher than EU and the US combined. Natural gas has a potential to advance in the industrial sector, mainly through coal-to-gas switching and as a feedstock for specific industries, such as petrochemicals and fertilizers industries.

The electricity generation sector, consuming 80 bcma, is notable for the dominance of coal with a 62% share of total electricity output, followed by hydroelectricity (14%), wind (9%), solar (6%), nuclear (5%) and natural gas (4%). China’s total electricity output is huge, representing one third of the global output. As such, even the relatively small share of China’s gas-fired electricity generation translates into 300 TWh output, which makes the country the fifth in the world in terms of gas-fired electricity output, lagging behind Iran, Japan, Russia, and the US. Gas-fired electricity growth is supported by the expansion of the relevant infrastructure, with gas-fired electricity capacity having recorded an unprecedented growth from 3 GW two decades ago to 130 GW in 2023, which is still smaller compared to 205 GW in the EU and 540 GW in the US.

The demand for natural gas in power generation is anticipated to grow robustly, driven by two factors. Firstly, China’s electricity sector, being one of the largest contributors to the country’s energy-related CO2 emissions (12.6 Gt in 2023, or 33% of the global volume), drastically needs a shift away from the over-reliance on coal-fired electricity output to tackle air pollution and mitigate emissions, with coal-to-gas switching providing such an opportunity. Second, natural gas may be highly needed to serve as a backup for renewables, which represent one third of China’s total electricity output and tend to expand their share. In particular, wind and solar need a backup power source because of their intermittency, while hydroelectric power needs a backup in case of lower hydro availability. Intermittency backup is envisaged by the Natural Gas Utilisation Policy, with “natural gas peak-shaving power station projects with a confirmed gas source and economic sustainability” included in the priority category for gas usage.

The residential sector, with 80 bcma of the domestic gas consumption, has been designated as the priority sector for gas usage by China’s government in all editions of Natural Gas Utilisation Policy. In its last edition, the government kept intact the priority status of gas usage for cooking and domestic hot water for urban residents, as well as centralized heating. The number of new residential clients of city gas firms has expanded consistently, having reached an incremental 10 million in 2022 and a further 8 million in 2023. Taking into account the number of households in the country, which still use high-carbon energy sources, mainly coal, gas consumption is likely to expand in this sector, in particular through coal-to-gas switching.

The transport sector is also witnessing an increase in the utilisation of gas. The country has long been the global leader with respect to natural gas vehicles, with strong uptake of compressed natural gas (CNG) as a fuel for passenger vehicles and liquefied natural gas (LNG) as a fuel for buses and long-range trucks. Furthermore, in the maritime industry, China has developed an extensive LNG bunkering infrastructure, which serves the refuelling of both ocean-sailing vessels, as well as vessels which traverse its own internal river networks.

To meet the growing domestic gas demand, China relies on both domestic gas production and gas imports, in the form of LNG and pipeline gas supplies.

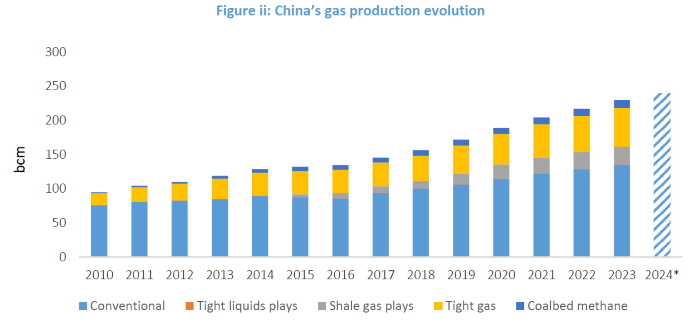

China’s gas production has witnessed a sustainable increase over the last two decades to reach 230 bcm in 2023, which is compared to 27 bcm in 2000 (Figure ii). As a result, China has become the fourth largest gas producer globally, after the US, Russia and Iran. Unconventional gas production, in particular shale gas and coal bed methane, is the main driver of the output growth, while representing 40% of total gas output. In particular, shale gas production reached 25 bcm in 2023, driven by the continuing development of the Sichuan Basin in the southwestern part of the country and supported by the national government’s incentives, in particular by reduced rates for resource tax valid from 2019 to 2027.

Source: GECF Secretariat based on data from Cedigaz

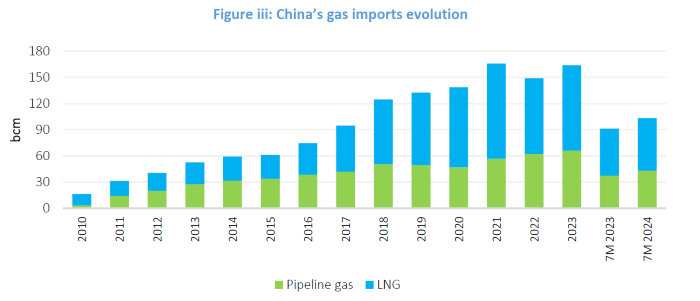

That said, the domestic gas production is capable of meeting only 60% of the domestic gas demand. In this context, China relies heavily on gas imports, which expanded nine-fold from 2010 to reach 164 bcm in 2023. Meanwhile, both LNG and pipeline gas supplies, which started in 2006 and 2010 respectively, have consistently increased (Figure iii). As a result, China has become the global leader in gas imports accounting for 16% of the world’s gas imports.

Source: GECF Secretariat based on data from Argus, General Administration of Customs China and Refinitiv

China has significantly increased LNG imports, which reached 72 Mt in 2023, with Australia, Qatar, Russia, Malaysia, and Indonesia being the leading LNG suppliers. China has become the largest LNG importer, accounting for 18% of global imports. In terms of regasification capacity, China also leads globally with over 140 Mtpa, with the average utilization rate of its 25 import terminals slightly above 50% and an additional 70 Mtpa of capacity expected to come online in the short term. It is worth noting recent changes in strategies of many global LNG exporters to the Chinese market, where some have increased the booking of LNG regasification capacity in China for the short, medium and long term, with a view to expanding their Chinese gas market access. Additionally, some global LNG exporters are signing long-term contracts not only with state-owned giants like CNPC, CNOOC and Sinopec, whom are increasingly interested in contractual-term LNG supply (inter alia, to expand their global LNG trading portfolio), but they are also signing contracts with smaller Chinese energy companies and end-consumers, with such agreements starting to dominate China’s LNG sales and purchase agreements recently.

China is also steadily expanding pipeline gas imports. The major supply comes from Central Asian countries, namely Turkmenistan, Kazakhstan and Uzbekistan, through the triple-line Central Asia - China gas pipeline with a combined capacity of 55 bcma. Russia is another major pipeline gas supplier to China, with flows going via the 38 bcma Power of Siberia pipeline, and the 10 bcma Far Eastern Route coming online by 2027. Moreover, China is holding negotiations with Turkmenistan on Line D of the Central Asia – China gas pipeline for an additional capacity of 30 bcma, and with Russia on the Power of Siberia 2 pipeline with incremental capacity of 50 bcma, transiting via Mongolia.

Given China’s commitment to its Nationally Determined Contributions (NDCs) and growing energy demand, driven by ambitious economic growth plans, natural gas has significant potential to increase its share in the domestic energy mix as a reliable complementary energy source to renewables and as a cost-effective replacement for coal. According to the GECF Global Gas Outlook 2050, natural gas demand in China is forecast to reach 530 bcm by 2030 and 670 bcm by 2050, securing one quarter of incremental global natural gas consumption. This growth will be supported by the country’s economic expansion, urbanisation, wealthier households, coal-to-gas conversions, infrastructure buildout, and ongoing market reforms.

In the meantime, China will continue to depend on gas imports because of the limited perspectives for domestic gas production growth. As such, the above-mentioned gas import capacity build-out will support China’s growing appetite for both LNG and pipeline gas imports, driven by its surging gas demand. China is expected to continue driving the growth in global gas imports in the short and medium term, which makes the country the priority market for many global gas exporters. In this context, it is worth mentioning that the GECF Member Countries together accounted for 42% of China’s total gas imports in 2023, in particular 49% of its LNG imports and 38% of its pipeline gas imports, and therefore they are well-positioned to strengthen their role in China's gas market in the short and medium term.