The global gas market has become increasingly affected by shifting weather patterns driven by the El Niño Southern Oscillation (ENSO). The ENSO is a recurring climate phenomenon that impacts atmospheric circulation by altering water temperatures in the Pacific Ocean, leading to fluctuations in air temperatures worldwide.

El Niño and La Niña represent two opposite cycles of ENSO. El Niño is characterized by warmer-than-normal sea surface temperatures in the central and eastern Pacific and weakened trade winds. This phase typically results in droughts across the western Pacific, especially in East Asia, and increased rainfall in the eastern Pacific, particularly in the Americas. El Niño also often leads to warmer-than-average winter temperatures in northern regions. On the other hand, La Niña is characterized by cooler-than-normal sea surface temperatures in the central and eastern Pacific, along with strengthened trade winds. This phase leads to heavier rainfall in the western Pacific and drought conditions in the eastern Pacific. Additionally, La Niña can result in colder-than-normal winters in northern regions and increased hurricane activity in the Atlantic. ENSO phases can last several months to over a year, with varying intensity and duration, making their global climate impacts difficult to predict.

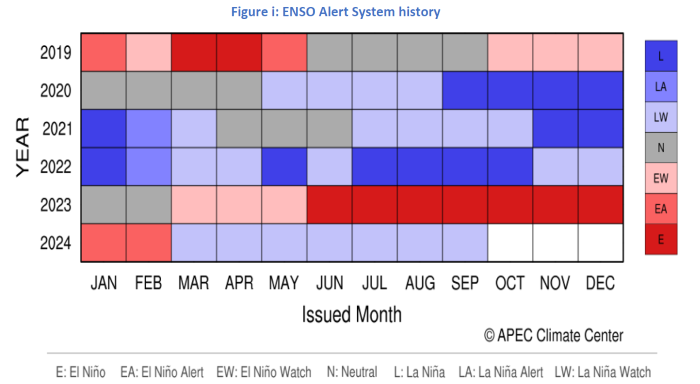

The ENSO Alert System is designed to monitor and forecast the phases of ENSO, providing regular updates on its status and issuing warnings based on current and predicted conditions. It features multiple alert levels, such as El Niño Event, El Niño Alert, El Niño Watch, Neutral, La Niña Watch, La Niña Alert, and La Niña Event, indicating varying degrees of likelihood and presence of ENSO conditions (Figure i).

Source: APEC Climate Center

The gas industry is highly sensitive to weather-driven fluctuations in demand, and ENSO events significantly impact gas consumption, production, and trade across various regions and sectors.

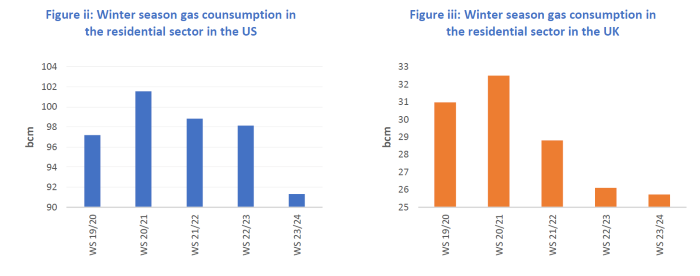

With regard to the residential / commercial sector, El Niño typically leads to warmer-than-average winters in the Northern Hemisphere, reducing gas demand in major gas-consuming regions such as Europe and North America, where natural gas is actively used for residential and commercial heating. Conversely, La Niña often brings colder-than-usual winters to these areas, sharply increasing the need for natural gas fuelled heating. Recent trends in gas consumption in the residential sectors of the US and UK during winter seasons highlight the direct influence of El Niño and La Niña events on gas demand. The winter season of 2020/2021 (WS 20/21), characterized by a strong La Niña event, saw the highest gas consumption in the residential sectors of both countries over the past five winter seasons (Figures ii and iii). In contrast, the 2023/2024 winter season, notable for reaching “Super” El Niño status — the sixth occurrence since 1950 — recorded the lowest gas consumption in both countries' residential sectors.

Source: GECF Secretariat based on data from US EIA, Ember and Refinitiv

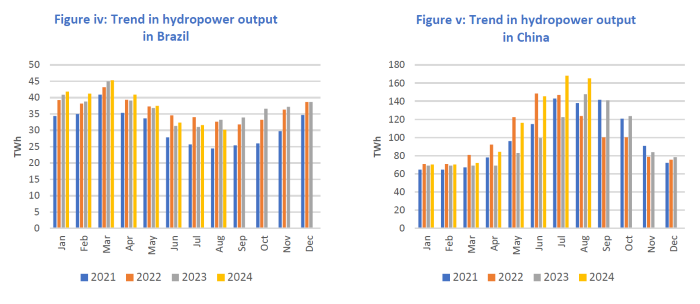

With regard to the electricity generation sector, both La Niña and El Niño have a significant impact on renewable energy output, particularly hydroelectric output, which is heavily reliant on precipitation levels. During El Niño, increased rainfall typically occurs across the Americas, while East Asia often experiences droughts. In contrast, La Niña usually brings droughts to the Americas and higher rainfall to East Asia. Drought conditions reduce hydroelectric generation, causing countries utilising significant hydro to rely more on natural gas for electricity, often turning to the spot LNG market to meet demand.

In the Americas, Brazil’s hydropower output declined to 363 TWh in 2021 during the La Niña cycle, leading to widespread droughts, while gas-fired power generation rose to 87 TWh. In contrast, during the 2023 El Niño, heavier rainfall boosted hydropower output to 429 TWh, reducing gas-fired power generation to 38 TWh. As a result, Brazil's LNG imports dropped from 10.3 bcm in 2021 to 1.2 bcm in 2023. With La Niña intensifying in 2024, Brazil recorded its first year-on-year decline in monthly hydroelectric production in August, with output falling by 3.1 TWh y-o-y (Figure iv). This decrease was partially offset by a 1.5 TWh y-o-y rise in gas-fired power generation. Ongoing droughts and low rainfall are expected to continue until December, likely leading to an increase in LNG imports.

In East Asia, China’s hydropower generation reached 1,300 TWh in 2021, the second-highest level on record, due to increased rainfall associated with La Niña. However, during 2023, hydropower output dropped to 1,226 TWh due to El Niño-induced droughts. This decline was offset by coal-fired and renewable generation, with growth in each segment exceeding 300 TWh, contributing to an overall electricity output increase of over 600 TWh. Gas-fired power generation also rose by 22 TWh that year. In 2024, with the return of La Niña and higher rainfall, China’s hydroelectric output has risen steadily, adding 165 TWh y-o-y in the first eight months of the year (Figure v).

Source: GECF Secretariat based on Ember data

The ENSO phenomenon also affects wind and solar power generation. El Niño typically reduces wind power output in many regions, while La Niña tends to enhance it, although the specific impacts depend on location and event intensity. ENSO phases also affect solar generation by altering cloud cover, sunlight intensity, and broader weather conditions.

Moreover, changes in global temperatures caused by El Niño and La Niña also affect gas-fired electricity generation. El Niño tends to increase air temperatures during summer in many regions, driving up cooling demand and, consequently, gas-fired power generation. For instance, in August 2023, the hottest August on record in many countries, including Brazil, China, Japan, Spain and the U.S., the prevailing El Niño significantly boosted gas-fired generation. However, with the shift to La Niña in Q2 2024, temperatures dropped across these regions through to August 2024.

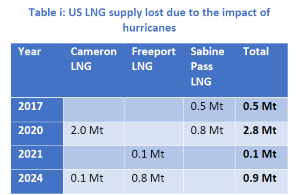

On the gas supply side, La Niña’s effect is primarily seen in the Atlantic basin, specifically in the Gulf of Mexico. With a high possibility of increased frequency and intensity of hurricanes in the event of La Niña, the gas production and LNG export infrastructure in the region are at risk of supply disruption due to outages and indirect impacts. For instance, operations at the Cameron and Sabine Pass LNG facilities were impacted by hurricanes in 2020, which was notable for a La Niña cycle, resulting in 3 Mt loss of LNG supply. In 2024, with the start of a La Niña cycle, the same LNG facilities have already been impacted by hurricanes, which led to the loss of almost 1 Mt of LNG supply (Table i). Moreover, amidst the reinforcing La Niña cycle, there is a risk of further disruptions to US LNG supply from intense hurricanes for the rest of the year.

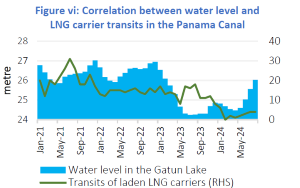

The ENSO phases also affect LNG shipping, particularly through the Panama Canal, where Gatun Lake provides water for the canal’s water gates to permit the transit of vessels of certain sizes. During the 2023 El Niño, reduced rainfall lowered water levels in Gatun Lake, prompting the Panama Canal Authority (PCA) to limit transits from September 2023. By February 2024, there were zero instances of laden LNG carriers transiting the canal (Figure vi). As a result, America’s LNG exporters had to reroute shipments to Asia via longer routes such as the Cape of Good Hope, increasing sailing times and costs. With weather patterns now shifting toward the La Niña cycle, rainfall has replenished Gatun Lake, allowing the PCA to ease transit restrictions and enabling a partial recovery of LNG carrier traffic.

Source: GECF Secretariat based on data from Argus, ICIS LNG Edge and Refinitiv Source: GECF Secretariat based on data from the Panama Canal Authority and ICIS

As of early October 2024, the ENSO Alert System indicated a La Niña Watch status, signalling a high likelihood (50% or greater) of a full La Niña event developing in the coming months. In the short term, this could lead to cooler-than-normal temperatures in the Northern Hemisphere during the upcoming winter season, increasing gas demand for heating. Simultaneously, drought conditions in the Americas, particularly in Brazil, may worsen, further diminishing hydroelectric generation and driving up the use of gas-fired electricity. In the long term, as the ENSO phenomenon continue to have an impact on weather patterns, natural gas is poised to maintain its role as a key fuel for heating in the residential and commercial sectors, and strengthen its position as a backup source for hydro, wind and solar electricity generation. To address the challenges posed by ENSO-related weather changes, it is crucial for governments and industries to develop effective strategies, prioritizing the security of gas supplies.