The transport sector, once regarded as a niche market for natural gas, is rapidly emerging as one of the potential demand growth areas. The adoption of LNG as a fuel for heavy-duty trucks with a load capacity exceeding 15 tonnes has gained momentum this year, driven by both environmental and economic factors.

From an environmental perspective, natural gas offers a significantly lower carbon footprint compared to traditional oil-based fuels. LNG-powered engines emit around 15% less CO2 over their lifecycle than diesel engines. Additionally, natural gas combustion substantially reduces sulphur and nitrogen oxides, virtually eliminates emissions of carcinogenic compounds and particulate matter, contributing to improved air quality.

In the transport sector, heavy-duty vehicles account for a significant share of energy-related CO₂ emissions. To address this challenge, many countries are actively promoting LNG-powered trucks, leveraging the environmental advantages of natural gas as a strategic measure to reduce greenhouse gas emissions and align with their Nationally Determined Contributions (NDCs).

From an economic perspective, the cost-competitiveness of LNG is driving the growing adoption of LNG-powered trucks in the automotive industry. It is generally considered that if the price of LNG is about 20% lower than diesel, market participants are incentivised to transition to LNG-powered trucks. Over the last decade, global LNG prices have remained lower than oil prices, except during the period from Q3 2021 to Q1 2023, when record-high gas prices temporarily undermined the competitiveness of LNG-powered trucks. Despite the higher upfront costs of LNG trucks—mainly due to the cryogenic fuel storage system— these costs are offset by lower LNG fuel prices and reduced maintenance expenses, offering significant long-term savings. This results in a more favourable payback period, often at least one year shorter than that of conventional diesel trucks. Furthermore, LNG holds distinct advantages over alternative fuels. It is more efficient than electric trucks for long-distance hauling, as the limited range of electric batteries makes them less suitable for long-range travel. LNG also outperforms CNG, thanks to its higher energy density, which enables longer distances between refuelling.

China stands as the global leader in the natural gas vehicle (NGV) market by a significant margin, dominating both the LNG and CNG segments. Environmental concerns are central to the Chinese government’s promotion of natural gas in the automotive sector. As the world’s largest emitter of energy-related CO2, with emissions reaching 11 Gt (representing 30% of global emissions), China has committed to achieving carbon neutrality by 2060 as part of its latest NDCs. In this context, NGVs are viewed as a critical component of China's decarbonization strategy, offering a more immediate solution compared to other sectors like power generation. Moreover, energy security considerations drive the promotion of NGVs, as China’s oil import dependency stands at 73%, much higher than its gas import dependency of 42%.

China, home to the world’s largest and most developed LNG-powered heavy-duty truck market, accounting for an estimated 80% share of the global market, introduced its first LNG-powered trucks in 2003. However, the number of LNG trucks remained modest in the first five years following their introduction.

Since 2008, energy policies driven by environmental concerns have played a key role in accelerating the growth of the LNG truck market. The 11th Five-Year Plan (2006-2010) for National Economic and Social Development in China emphasized “the development and use of energy-saving, environmentally friendly and new fuel vehicles”. This policy paved the way for the real growth of the LNG truck market, with the fleet reaching 30,000 vehicles in 2008. These energy policies are implemented through various government support mechanisms, including subsidies for fuel, truck scrapping, and refuelling infrastructure.

Fuel subsidies are a notable feature, with natural gas fuels, including LNG, being exempt from various taxes. In contrast, diesel and gasoline are subject to high taxes, including consumption and value-added taxes, which together can account for up to 40% of the retail price. Additionally, the government runs a truck scrapping program that encourages the retirement of older, more polluting heavy-duty trucks. Under this program, fleet owners can receive up to $11,000 when replacing an old truck with one powered by low-emission fuels like LNG. Moreover, subsidies are also available for the construction of LNG refuelling infrastructure, which is crucial for expanding the market. As of now, there are more than 5,000 LNG refuelling stations across China supported mainly by over 80 domestic liquefaction plants, which are supplied by local gas fields. In this context, the lower, more stable production costs make LNG fuel in China less susceptible to global price fluctuations. A major part of these stations and plants are in the northern provinces. In the meantime, imported LNG is also used for truck refuelling, although in much smaller volumes, particularly in southern and eastern regions, where most of the 30 domestic LNG import terminals operate.

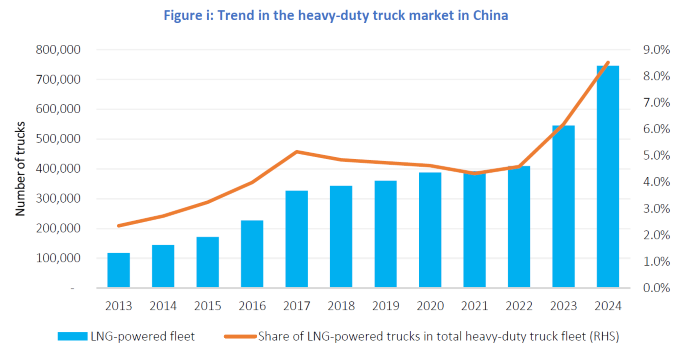

By 2022, China’s LNG-powered truck fleet exceeded 450,000 vehicles. The market saw explosive growth following the introduction of updated automotive regulations in July 2023. These regulations, which included stricter limits on nitrogen oxide and particulate matter emissions from heavy-duty trucks, also required new trucks to install anti-tampering monitoring systems and remote diagnostics to ensure compliance with real-world emissions standards. This made LNG-powered trucks, which already meet these stringent requirements, more attractive to fleet operators.

Economic factors have also been a significant driver of market’s growth. The price difference between diesel and LNG fuel has recently become again more favourable for LNG. By November 2024, the average diesel price for heavy-duty trucks in China was around 7.10 yuan/litre, while the average LNG fuel price was approximately 4.80 yuan/kg. Assuming that both diesel and LNG trucks consume roughly the same amount of fuel — around 40 litres of diesel and 40 kg of LNG fuel per 100 km — fleet operators can save around 140,000 yuan (up to $20,000) per year in fuel costs by switching from diesel to LNG.

With both favourable energy policies and economics, China has seen an unprecedented surge in LNG-powered truck sales, particularly since the second half of 2023. In the first three quarters of 2024 alone, approximately 150,000 LNG-powered trucks were sold, representing 35% of total heavy-duty truck sales, a sharp increase from just 4% in 2022. Since 2022, the sale of new trucks has largely been driven by the need to replace older vehicles, with more than 600,000 heavy-duty trucks being replaced annually. This trend has further boosted the adoption of LNG-powered trucks. As a result, the number of LNG-powered trucks in operation in China is now estimated at around 750,000, with their share in the country’s total heavy-duty truck fleet almost doubling from 4.6% in 2022 to 8.5% in 2024 (Figure i). If the current sales trajectory continues, China’s LNG-powered truck fleet is expected to exceed one million vehicles by the end of 2025. With LNG rapidly gaining market share, it is set to become a dominant fuel alongside diesel in China’s heavy-duty truck market.

Source: GECF Secretariat estimates based on data from China Association of Automobile Manufacturers, CIECData, McKinsey, Bloomberg and Energy Intelligence

Various countries around the world are looking to replicate China’s success and follow suit in adopting LNG as a fuel for trucks.

India, for example, is actively promoting LNG in its truck market as part of its broader transition to a gas-based economy. The country aims to increase the share of natural gas in its primary energy mix from the current 6% to 15% by 2030. Although India currently has fewer than 1,000 LNG-powered trucks, which represent only a small fraction of its 7 million truck fleet, the government plans to have one-third of the truck fleet running on LNG within the next five to seven years. India's high oil import dependency, which exceeds that of China, provides an additional incentive for this shift. To support it, the government is focusing on expanding LNG refuelling infrastructure, which remains limited, and earmarking volumes of domestic gas — cheaper than imported LNG — for LNG-powered trucks.

In the EU and the US, which have been pioneers in adopting LNG as a fuel for trucks, significant progress has been made. The EU currently has around 30,000 LNG-powered trucks and 750 LNG refuelling stations, mainly supported by high-volume LNG import infrastructure. Germany, Italy, Spain, and France are the leading countries, accounting for three-quarters of the regional market. In the US, approximately 25,000 LNG-powered trucks are in operation, supported by 50 LNG refuelling stations. The market has considerable growth potential, particularly as LNG production projects continue to be developed.

GECF Member Countries, which hold vast natural gas reserves, are also well-positioned to increase the use of LNG fuel. Some of these countries already have established LNG truck markets, while others are planning to launch dedicated programs to expand LNG adoption.

LNG offers a cleaner and more cost-effective alternative to traditional fuels, especially for heavy-duty trucks. China has solidified its position as the global leader in this sector, with government policies and economic incentives driving the growing adoption of LNG-powered trucks. Other countries are looking to replicate this model by addressing challenges such as limited refuelling infrastructure. The upcoming expansion of global LNG export capacity is expected to help stabilize prices and support further growth in the LNG-powered truck market, particularly in countries dependent on gas and LNG imports. In this context, GECF Member Countries are well-positioned to help drive the global expansion of LNG-powered trucks.