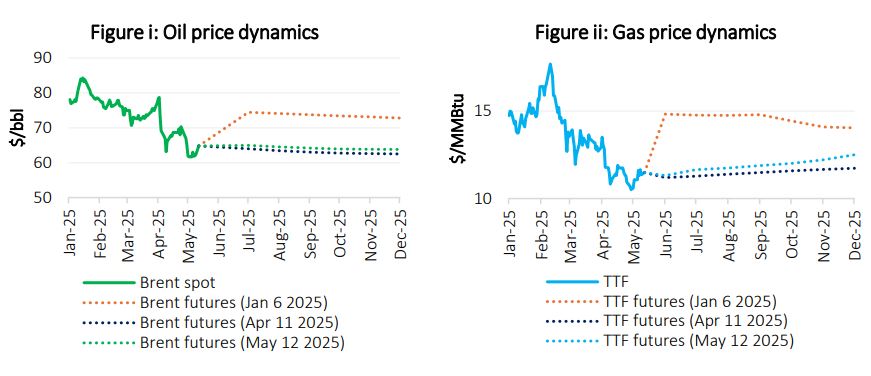

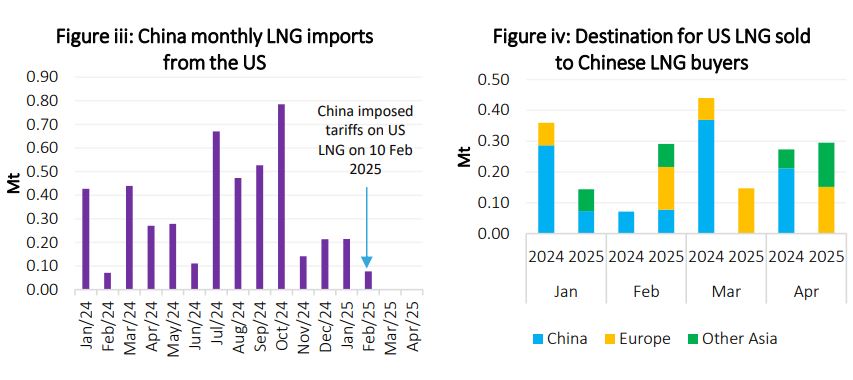

The recent dramatic shift in US tariff policy has led to heightened global economic volatility and uncertainty, affecting a wide range of sectors, including energy and gas markets. As the world’s largest importer of goods with $3.2 trillion in imports in 2024 (13% of global imports), the US has a huge potential to impact global trade and overall economic growth with any major changes in its trade policy, particularly in the area of tariffs. The expanding US trade deficit, which reached $1.2 trillion in 2024, has been a key driver behind the introduction of new tariffs aimed at narrowing the imbalance and protecting domestic industries. Notably, 42% of US imports in 2024 originated from just three countries — Mexico, China, and Canada — with the combined trade deficit with these partners reaching $530 billion, or 45% of the total US trade deficit. Historically, U.S. tariff policy has supported trade liberalization, maintaining an average tradeweighted tariff rate below 4% since the early 1970s. However, on 2 April 2025, the US administration announced a sweeping change: a baseline 10% tariff on imports from 185 countries, along with higher country-specific tariffs — ranging from 17% to 49% — on 83 countries. With the exception of the UK, all major US trading partners have been subjected to these elevated country-specific tariffs. China, in particular, would be subject to the most severe measures, with tariff rates increased to 145%. If the announced tariffs were fully implemented, these measures could have raised the average effective US tariff rate to 25%, representing a dramatic departure from decades of liberal trade policy and effectively repositioning the US as one of the most protectionist economies globally. Nevertheless, it is worth noting that imports of energy and energy-related products — including oil, gas, and refined petroleum — were exempted from the new tariff regime. Global financial markets experienced sharp declines following the US tariff announcement on 2 April 2025. By 7 April, the S&P 500 and NASDAQ 100 had each dropped by 11%, while Japan’s NIKKEI 225 fell by 13% and Europe’s STOXX index declined by 12%. Commodity markets also came under significant pressure. In the oil market, Brent spot prices declined notably, driven by growing concerns over weakening global oil demand, further intensified by OPEC+’s announcement of a production increase set to begin in May 2025 (Figure i). In the gas market, TTF spot prices fell by 10% by 7 April 2025, largely due to expectations of reduced gas demand from industrial and power generation sectors. As of 12 May 2025, TTF spot prices are now projected to average $12.4/MMBtu for 2025 (down from the earlier forecast of $14.7/MMBtu issued on 6 January 2025) and $11.4/MMBtu for 2026 (Figure ii). The escalation of US tariffs, as initially announced, along with retaliatory measures from key trading partners, are expected to suppress global trade flows and contribute to a broader deceleration in economic activity. According to the IMF's latest forecast, published on 22 April 2025, the global GDP growth projection for 2025 based on purchasing power parity (PPP) has been revised downward from 3.3% (as forecast in January 2025) to 2.8%. Notably, the US economic outlook was downgraded from 2.7% to 1.8%, while China’s forecast was adjusted from 4.6% to 4.0%.

Source: GECF Secretariat based on data from LSEG

However, following the announcement of the new US tariffs, the situation has taken new turns, marked by several important developments. On 9 April 2025, the US government announced a 90-day suspension of the newly introduced tariffs for all countries except China, allowing time for trade negotiations and further policy review. Subsequently, the US has made progress in trade discussions with multiple partners. Most notably, on 12 May 2025, the US and China announced a breakthrough agreement to temporarily roll back tariffs for an initial 90-day period. Under the terms of the agreement, the US will reduce its tariffs on Chinese goods from 145% to 30%, while China will lower its tariffs on US imports from 125% to 10%. This marks a significant de-escalation in trade tensions between the world’s two largest economies and may set the stage for further dialogue on long-term trade cooperation. Gas markets have been affected by tariff policy escalations, both directly and indirectly, resulting in the rerouting of LNG cargoes, shifts in trade dynamics, and heightened uncertainty surrounding long-term investment decisions. Following China’s imposition of a 15% retaliatory tariff on US LNG imports on 10 February 2025, shipments of US LNG to China have ceased entirely (Figure iii). Subsequent increases in China’s tariffs have further elevated the delivered cost of US LNG, rendering it entirely uncompetitive in China. In this context, several Chinese LNG buyers holding long-term sales and purchase agreements with US LNG suppliers have increased trading activities outside China, redirecting US LNG cargoes to alternative markets, particularly to Europe and other parts of Asia (Figure iv). The inherent destination flexibility of US LNG has enabled this redirection, allowing suppliers to optimize deliveries in response to shifting trade dynamics. In the meantime, the US–China agreement on 12 May 2025 to ease reciprocal tariffs, under which China reduced its tariff on US goods to 10%, may pave the way for a potential resumption of US LNG imports in China. With the lower tariff, the delivered cost of contractual US LNG is now below prevailing spot LNG prices. Despite this, the extent of any recovery in US LNG flows to China will largely depend on China’s overall LNG demand, which has been declining in recent months amid rising domestic gas production and increased pipeline gas imports.

Source: GECF Secretariat based on data from ICIS LNG Edge

The US aims to leverage its LNG exports as a strategic tool to reduce its trade deficit with key trading partners, particularly in Asia. Nearly 100 Mtpa of LNG liquefaction capacity is currently under construction in the US, with an additional 115 Mtpa targeting FIDs in the near term, largely contingent upon securing new long-term LNG contracts. Since the imposition of US tariffs, several Asian countries have expressed interest in increasing their LNG imports from the US as a means to narrow their trade surpluses. In parallel, energy companies from Japan, South Korea, Taiwan, and Thailand have shown interest in participating in the 20 Mtpa Alaska LNG project. The newly introduced 25% industry-specific tariff on steel and aluminium imports in the US, if remain in effect, will pose a potential challenge to the cost competitiveness of US LNG projects. Materials and equipment based on steel and aluminium account for 15-30% of the total cost of an LNG plant. If all such materials are imported and represent 30% of project costs, the tariff could increase total capital expenditure by up to 7.5%, or even higher if the impact of the retaliatory tariffs and the induced inflation are taken into account. This added cost may reduce the profitability of US LNG projects currently under construction or targeting FID, with around 50 Mt of liquefaction capacity at pre-FID stage being at risk. In response, developers already try to renegotiate liquefaction fees in sales and purchase agreements to preserve margins. Moreover, US tariffs on imported steel and aluminum are expected to raise material and equipment costs for upstream and pipeline infrastructure projects, driving up the cost of gas supply in the domestic market, which, in turn, would increase the price of feed gas for liquefaction plants. Higher project costs also heighten financial risks and hedging expenses, making US gas producers more vulnerable to market volatility. The potential impact of US tariffs on global gas demand is expected to vary by sector and region. Sectorally, the industrial sector is likely to experience the sharpest decline, particularly in gasintensive industries. Power generation could also see a moderate reduction in gas demand, driven by slower-than-expected GDP growth. In contrast, demand in the residential, commercial, and transport sectors is expected to remain relatively stable, as these segments are generally less sensitive to economic fluctuations. Regionally, gas consumption in Asia Pacific, Europe, and the US may decline due to a slowdown in industrial activity.

In addition to tariff interventions, the US is pursuing other protectionist policies that may impact gas markets. One key initiative is the administration’s ambition to revitalize the domestic shipbuilding industry, particularly in the LNG carrier segment. A proposed measure includes a phased requirement for US LNG exports to increasingly rely on domestically built, flagged, and operated ships, starting with a 1% quota in 2028 and rising incrementally to 15% by 2047. Although not yet enacted, this proposal reflects a strategic shift toward boosting national industrial capabilities. Given that the current global LNG fleet is largely composed of foreign-built and foreign-flagged vessels, and considering the US limited capacity to manufacture LNG carriers, such a policy could significantly increase transportation costs for US LNG supply. This may undermine the competitiveness of US LNG, particularly in pricesensitive regions outside Europe. Furthermore, the US administration has proposed the imposition of port fees on Chineseowned, operated, or built ships making port calls in the US, intended as a direct economic disincentive targeting Chinese maritime trade. While these proposed fees are not specifically aimed at the gas sector, they could indirectly impact global gas markets by increasing LNG shipping costs and adding logistical complexity. If implemented starting in October 2025, the escalating fees may discourage the use of Chinese maritime assets in US LNG transport, potentially raising chartering costs or forcing rerouting in an already constrained LNG shipping market. This would increase the delivered cost of US LNG to China and to other regions reliant on Chinese shipping capacity. Moreover, regulatory uncertainty surrounding such measures could deter Chinese companies from investing in or committing to long-term US LNG contracts. Retaliatory action by China, such as imposing similar port fees on US-flagged vessels or energy imports, could further escalate trade tensions, compounding risks for global LNG trade flows and long-term investment planning.