Gas storage plays a vital role in the global gas market, serving as a stabilizing buffer against imbalances caused by seasonal demand patterns and unexpected supply disruptions. Storage also helps mitigate market volatility during periods of price swings driven by external shocks, such as geopolitical events or natural disasters, by ensuring continuous and reliable gas supplies. Maintaining an adequate level of gas storage allows both consumers and suppliers to navigate periods of uncertainty, enhancing stability and resilience across the energy sector.

The EU is the second largest region in terms of underground gas storage (UGS) capacity, behind the US. EU member states collectively operate UGS sites with a working gas capacity of 104 bcm, accounting for one quarter of the global capacity. The importance of gas storage in the EU has grown significantly since the 2022 energy crisis, underscoring the need for supply security and system flexibility. Storage is especially critical given the region’s sharp seasonal demand swing, with winter gas consumption rising by circa 135% compared to the summer. This contrasts with a 50% seasonal increase in the US and just 11% in China, highlighting the EU’s heightened dependence on storage for winter supply reliability.

In June 2022, the EU underwent a structural shift in its gas market framework with the adoption of Regulation (EU) 2022/1032, aimed at ensuring stable gas supply in winter seasons. This regulation introduced three key measures for EU member states to enhance gas storage security. First, it set binding capacity targets for UGS sites: storage facilities were to be filled to at least 80% by 1 November 2022, increasing to 90% by 1 November in subsequent years. Intermediate targets were also established throughout the year, specifically at the start of February, May, July and September. Second, the regulation limited the required filling volume to 35% of the member state’s average annual gas consumption over the previous five years. This provision aimed to prevent disproportionate burdens on countries like Austria, which have relatively low consumption but large storage capacity. Third, member states without UGS facilities were granted access to storage in other member states, equivalent to up to 15% of their average annual gas consumption over the past five years. This measure ensured fair access and regional solidarity within the internal energy market.

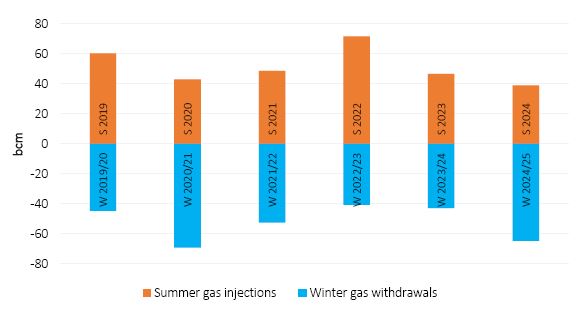

The new regulation prompted EU member states to inject a record 72 bcm into UGS facilities during the 2022 summer season, following a historically low end-of-winter level of just 26 bcm. That enabled the region to maintain a reliable gas supply throughout the 2022/2023 winter. In both 2023 and 2024, the EU encountered fewer challenges in meeting its intra-year storage targets, owing to a combination of factors: milder-than-expected winter weather, declining gas demand, robust LNG imports, and stabilised pipeline gas imports. These conditions contributed to net gas withdrawals of just 41 and 43 bcm over the two winter seasons, the lowest levels in over a decade. By the end of the 2023/2024 winter, gas storage remained at an all-time high of 61 bcm. As a result, gas injection needs during the 2024 summer season were significantly reduced, with only 39 bcm injected, marking a record low since 2012 (Figure i).

Figure i: UGS injections and withdrawals in the EU

Source: GECF Secretariat based on data from AGSI+

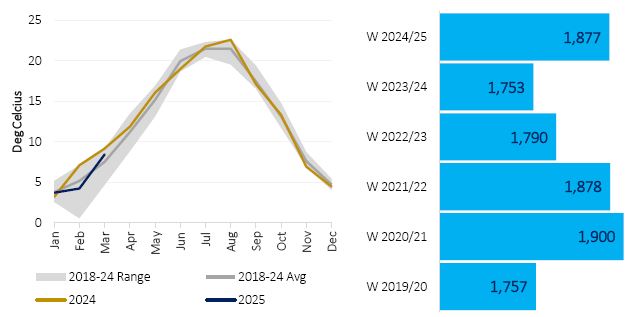

However, after two consecutive winters of milder-than-average temperatures, the 2024/2025 winter marked a return to colder weather conditions, last seen three years ago. Net gas withdrawals began as early as 22 October 2024, more than two weeks earlier than in 2023, and average EU temperatures remained below historical norms throughout the winter. During the core winter months (November 2024 to March 2025), the average temperature in the EU dropped to 5.6°C, significantly lower than 6.5°C in 2023/2024 and the average of the previous six winters of 6.0°C. This is supported by heating degree days (HDDs) data, which measure heating demand by calculating the difference between the mean daily temperature and a reference temperature. Over the 2024/2025 winter season, the EU recorded a total of 1,877 HDDs, representing a 7% increase compared to the previous winter and a 3% increase over the average of the prior six winter seasons (Figure ii).

Figure ii: Average EU temperatures (left) and heating degree days (right)

Source: GECF Secretariat based on data from LSEG

Below-average temperatures during the 2024/2025 winter posed challenges to the supply-demand balance in the regional gas market. On the demand side, colder weather led to a significant increase in gas consumption for heating, with the region estimated to have consumed 16 bcm more than during the previous winter.

On the supply side, the EU experienced reduced gas availability, driven by declines in both domestic production and gas imports. Domestic output continued its structural downward trend due to depleting reserves, with the total domestic EU output declining from 17 bcm in the 2021/2022 winter to 12 bcm in the 2024/2025 winter, hence, further intensifying the region’s dependence on external supply. However, pipeline gas imports during the winter season fell sharply by 42 bcm over the past three years, from 104 bcm in 2021/2022 to 62 bcm in 2024/2025, largely as a result of geopolitical developments. This decline was only partially offset by a 12 bcm increase in LNG imports during the winter season, rising from 43 bcm in 2021/2022 to 55 bcm in 2024/2025. Consequently, total EU gas imports dropped to 117 bcm during the 2024/2025 winter, down from 121 bcm in 2023/2024, 123 bcm in 2022/2023 and 147 bcm in 2021/2022, further aggravating the region’s supply situation amid heightened seasonal demand.

With the supply-demand balance tightening, the EU was forced to rely on UGS withdrawals during the 2024/2025 winter as a critical component of gas supply, with withdrawals reaching 65 bcm, a level not seen since 2020/2021. As a result, storage levels fell to just 35 bcm by the end of the winter season. While this is only slightly below the 10-year average of 38 bcm, it is significantly lower than the levels recorded in 2024 (61 bcm) and 2023 (57 bcm), making the current gas storage situation markedly different and considerably more complex.

By 1 November 2025, under the current gas storage regulations, EU member states must restock approximately 60 bcm to meet the 90% capacity target. This figure is significantly higher than the volumes injected during the 2023 and 2024 summer seasons, which amounted to 47 bcm and 39 bcm, respectively. Given the anticipated decline in pipeline gas imports and the continued tightness in the global LNG market, the EU may face considerable challenges in achieving this target within the required timeframe.

The common expectation is that the EU will succeed in injecting the required storage volumes, however, compliance with mandatory storage targets is likely to lead to elevated prices, as was the case during the 2022 energy crisis. At that time, Europe, urgently seeking LNG to offset declining pipeline gas imports, emerged as a premium destination for global LNG, overtaking Asia. This was reflected in European hub prices surpassing Asian spot LNG prices, marking an unprecedented reversal of the traditional inter-regional price relationship. As market conditions stabilized, the NEA-TTF price spread gradually returned to historical norms, with Asia regaining its premium over Europe in 2023 and 2024. In 2025, as Europe once again demands higher LNG volumes to refill UGS sites, and therefore competes with Asia for spot LNG cargoes, TTF spot prices are expected to remain elevated throughout the summer. Additionally, lower-than-expected LNG demand in China and the US-initiated tariff war may exert downward pressure on spot LNG prices in both regions.

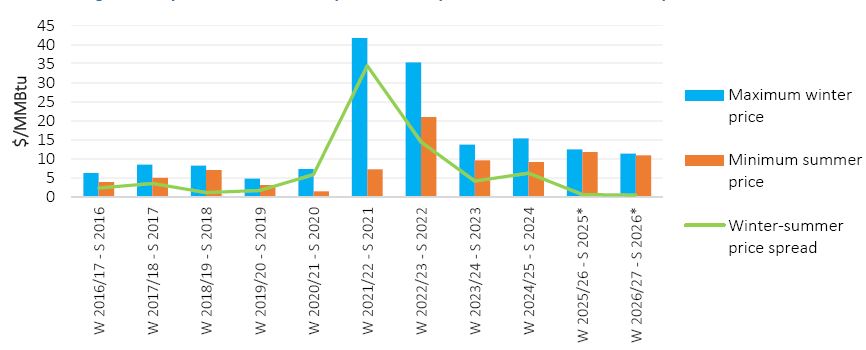

Moreover, there is a strong correlation between gas prices and storage dynamics in the EU market. During the winter months, colder temperatures drive up heating demand, leading to higher gas consumption and a corresponding increase in prices. Conversely, in the summer, heating demand declines sharply, resulting in lower consumption and typically lower prices. This seasonal pattern generates a winter-summer price spread, incentivizing market operators to buy gas at lower summer prices, inject it into UGS sites, and resell it in winter at higher prices.

Considering the maximum average monthly TTF price during the winter months versus the minimum average monthly TTF price during the summer months, the seasonal price spread averaged $2.9/MMBtu between 2016 and 2020 (Figure iii). Amidst the post-pandemic recovery and the 2022 energy crisis, the spread widened to an unprecedented $35/MMBtu in 2021 and $14/MMBtu in 2022, and remained at an economically effective level of $4–6/MMBtu in 2023 and 2024. However, in 2025, futures price dynamics indicate a slightly positive winter-summer price spread of just $0.7/MMBtu, as the EU’s gas storage regulations are expected to support high injection demand, exerting upward pressure on prices. At the same time, the global gas market is expected to see increased supply by year-end, with 54 Mtpa of new liquefaction capacity coming online throughout 2025 and production ramping up by year-end, which is likely to suppress any significant rise in winter prices. As a result, the narrow seasonal price spread is expected to lead to commercial losses for gas storage operations.

Figure iii: Spread between the peak winter prices and lowest summer prices in the EU

Source: GECF Secretariat based on data from AGSI+ and LSEG

Note: Prices from May 2025 are based on TTF futures as of 21 April 2025

Regulation (EU) 2022/1032 was initially set to expire at the end of 2025, but in March 2025, the European Commission proposed a two-year extension, through the end of 2027, emphasizing its continued importance for ensuring both gas supply security and market stability. At the same time, the Commission is reviewing proposals from several member states seeking greater flexibility within the regulatory framework, particularly by allowing 10% deviations from storage targets and compliance deadlines under exceptional national circumstances. Looking beyond 2027, the EU gas market is expected to evolve toward a more balanced and resilient structure, potentially reducing the need for such administrative.